Most homeowners discover the hard way that "rebuild cost" means far more than construction. Debris removal, hazmat remediation, soil testing, permits, code compliance upgrades, and months of temporary housing all land before — or alongside — a single framing nail. Budget only for construction, and you'll run out of money mid-project.

This guide breaks down every cost layer of rebuilding after a California wildfire, so you can plan with clarity.

Key Takeaways

- Total rebuilding costs in California typically range from $300,000 to over $1 million for a single-family home

- Pre-construction phases — debris removal, permits, soil testing, engineering — commonly consume $75,000–$200,000 before construction begins

- WUI code-compliant upgrades added $13,070 to a 1,750 sq ft Altadena home, per a 2025 Headwaters/IBHS study

- Post-disaster demand surge pushes contractor and material prices well above pre-fire market rates

- Building to higher resilience standards costs less than 10% more but can reduce destruction risk by up to 43%

What Does Rebuilding After a Wildfire in California Actually Cost?

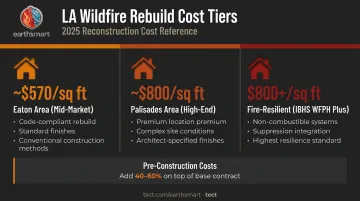

Rebuild costs in California range from roughly $570 to $800+ per square foot — but that number shifts significantly based on location, fire severity zone, market conditions, and build standard. No two projects land in the same place.

Two cost traps consistently catch homeowners off guard:

- Underestimating pre-construction expenses — debris removal, hazmat remediation, soil testing, engineering, and permits routinely consume $75,000–$200,000 before construction begins

- Ignoring post-disaster demand surge — when thousands of homes burn simultaneously, contractor and material prices rise sharply above pre-fire market rates

Typical Rebuild Cost Ranges

Owner-reported estimates cited by the LA Times from the 2025 fires show a wide spread depending on location and complexity:

| Rebuild Tier | Reported Range | What's Included |

|---|---|---|

| Eaton area (mid-market) | ~$570/sq ft | Code-compliant rebuild, standard finishes |

| Palisades area (high-end) | ~$800/sq ft | Premium location, complex sites, higher finish standard |

| Fire-resilient (IBHS WFPH Plus) | ~$800+/sq ft | Non-combustible systems, suppression integration, long-life assemblies |

These are owner estimates from reported cases, not cost-database figures — so use them as directional reference points. Across all tiers, one pattern holds: raw construction is only part of the bill. Pre-construction, permits, temporary housing, and finishes regularly add 40–60% on top of the base contract.

Key Factors That Drive Rebuild Costs Higher in California

Wildfire rebuild costs are shaped by regulatory requirements, market conditions, site complexity, and home specifications. Most of these factors push costs above standard new construction in other states.

Fire Severity Zone and Code Requirements

Homes in CAL FIRE-designated High Fire Hazard Severity Zones must comply with California's Wildland-Urban Interface Code (Title 24, Part 7, effective January 1, 2026). Requirements include:

- Class A roofing

- Flame- and ember-resistant vents

- Noncombustible or ignition-resistant exterior wall materials

- Dual-pane glazing with at least one tempered pane

- Fire sprinklers (required statewide for new one- and two-family dwellings under California Residential Code R313)

A 2025 Headwaters Economics/IBHS study found that meeting WUI code requirements added $13,070 to a 1,750 sq ft Altadena model home versus traditional construction.

Home Size and Complexity

Cost scales with square footage, but also with:

- Roof pitch and complexity

- Number of stories

- Deck square footage

- ADU presence

- Exterior surface area (which directly affects WUI code upgrade costs)

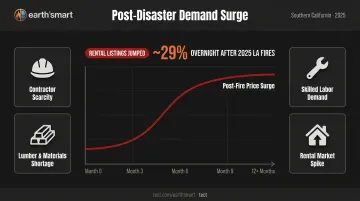

Demand Surge Pricing

When thousands of homes burn at once, demand for contractors, lumber, drywall, and skilled labor far outpaces supply. The California Department of Insurance formally defines demand surge as the post-disaster price increases that occur when contractors and materials become scarce. After the 2025 fires, Reuters reported that rental listings in affected areas jumped nearly 29% overnight — construction pricing faces similar dynamics.

Homeowners who delay rebuilding are not protected from these increases. Material and labor prices can remain elevated for 12 months or more after a major disaster.

Site Complexity and Location

Hillside lots, narrow access roads, and contaminated soils — common in WUI communities like Pacific Palisades — add substantial cost compared to flat suburban parcels. These factors affect foundation engineering, logistics, and site preparation in ways that require geotechnical work to pin down.

Permitting and Regulatory Timelines

Those site and code costs compound when permitting takes longer than expected. LA County accelerated its review process after the 2025 fires, with official targets now set at:

- 10 business days for initial Building and Safety/Fire Department review

- 5 business days for rechecks

- 2 weeks for Regional Planning initial review and recheck

Delays still occur. Each month of delay extends temporary housing costs and exposes locked-in material prices to further inflation.

The Full Cost Breakdown: What You're Really Paying For

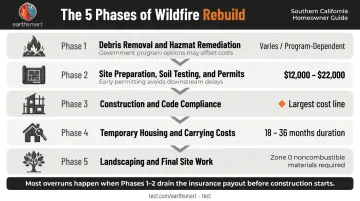

Total rebuild cost is the sum of five sequential phases. Most cost overruns happen because homeowners budget for Phase 3 while Phases 1 and 2 quietly drain their insurance payout first.

Phase 1 — Debris Removal and Hazmat Remediation

Before any rebuild can begin, the lot must be fully cleared of fire debris, contaminated soil, hazardous materials (asbestos, lead paint, household chemicals), and often the original foundation.

The government program option: LA County's Phase II debris removal through the Army Corps of Engineers has no direct cost to the owner for eligible participants. Phase I hazmat removal was completed by February 27, 2025, and the Army Corps has since cleared thousands of parcels. Enrolled homeowners must assign insurance proceeds designated for debris removal to avoid duplication of benefits.

If you opt out or are ineligible: Private debris removal costs are substantial. For context, CalRecycle's Camp Fire debris removal contract for approximately 2,000 parcels in Paradise carried an estimated cost of $200 million — roughly $100,000 per parcel on average.

Check your policy's debris removal limit before assuming the government program covers everything. CDI confirms that standard policies typically cap debris removal at 5% of the dwelling coverage limit.

Phase 2 — Site Preparation, Soil Testing, and Permits

After lot clearance, counties often require geotechnical review before issuing rebuild permits. LA County triggers a compaction report if the slab or foundation is demolished and soil is disturbed more than 12 inches. Additional soils reports are required for caissons, deep piles, geologic hazards, or basement walls.

LA County permit cost benchmarks (official):

- ~$12,000 for a 1,500 sq ft home

- ~$22,000 for a 3,000 sq ft home

- $1,404 for like-for-like residential rebuilds through Regional Planning

Fees may be waived for qualifying homeowners rebuilding single-family homes. Confirm eligibility through the LA County Recovers portal.

Phase 3 — Construction and Code Compliance Upgrades

This is the largest single cost line. For homes in mapped high-hazard zones, California's WUI Code (Part 7) mandates specific assemblies and materials across every system:

- Fire-resistive wall assemblies and roofing

- Non-combustible exterior cladding and vents

- Integrated suppression systems

- Upgraded electrical and HVAC to current code

If you carry Ordinance or Law coverage on your homeowners policy, that coverage is specifically designed to fund these required upgrades. Many homeowners discover after a loss that they either carry no Ordinance or Law coverage or carry limits far below what the upgrades actually cost.

Coordinating WUI compliance systems before materials are specified — not mid-project — is where teams like earth'smart powered by tect add the most value. Through the earth'smart powered by tectApp™ community of 70+ building product manufacturers, earth'smart powered by tect engages the right product experts during design, so fire-resistive assemblies and suppression systems are integrated correctly from the start rather than corrected at greater cost later.

Phase 4 — Temporary Housing and Carrying Costs

Displaced homeowners carry housing costs throughout the entire rebuild timeline. The LA rental market was severely stressed after the 2025 fires, with documented price gouging — Reuters reported one Beverly Hills rental jumped nearly 29% overnight, and LA sued Airbnb alleging over 2,000 listings rose more than 10% after the fires.

CDI protections: Insurers were ordered to advance at least 4 months of Additional Living Expenses immediately, and survivors have at least 36 months to collect ALE with possible 6-month extensions.

Full rebuild timelines in California post-wildfire commonly run 18–36 months from lot clearance to occupancy, depending on permitting speed, contractor availability, and project complexity. At current LA-market housing costs, that temporary housing exposure adds up fast.

Phase 5 — Landscaping, Defensible Space, and Final Site Work

The final phase includes:

- Defensible space landscaping (legally required to 100 feet under PRC 4291)

- Hardscape and driveway restoration

- Utility reconnections

- Final inspections

Zone 0 (0–5 ft from the structure) is particularly important — and requires noncombustible materials rather than wood mulch or combustible plantings. A 2025 Headwaters/IBHS model found Zone 0 noncombustible landscaping costs approximately $3,742, compared to $1,106 for traditional bark mulch and wood fencing. Homeowners who skip compliant landscaping risk insurance non-renewal or local citation.

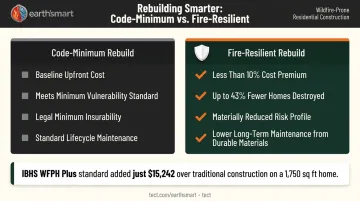

Standard Rebuild vs. Fire-Resilient Rebuild: What's the Difference?

After a total loss, the instinct is to rebuild quickly and affordably. A code-minimum rebuild accomplishes that, but it also restores the same vulnerability level that existed before the fire.

Side-by-Side Comparison

| Dimension | Code-Minimum Rebuild | Fire-Resilient Rebuild |

|---|---|---|

| Upfront cost premium | Baseline | Less than 10% more |

| Destruction risk reduction | Meets minimum standard | Up to 43% fewer homes destroyed |

| Insurability | Meets legal minimum | Materially reduces risk profile |

| Long-term maintenance | Standard lifecycle | Lower, due to durable material systems |

The Headwaters Economics/IBHS 2025 study found that the IBHS Wildfire Prepared Home Plus standard added just $15,242 over traditional construction on a 1,750 sq ft Altadena model — less than 10% above baseline, with substantially better performance outcomes.

What Fire-Resilient Construction Actually Involves

Going beyond minimum code means specific material and system choices:

- Pre-insulated concrete masonry for exterior wall systems (versus wood framing)

- Non-combustible materials throughout, not just at code-required locations

- Long-life roofing systems engineered for fire, flood, and seismic exposure

- Integrated on-site water supply for fire events, paired with site-scale suppression (vapor dome systems)

- Fresh, filtered air systems for habitability during fire events

Capturing this value without cost overruns comes down to one factor: making these decisions before materials are specified and contractors engaged. Early coordination locks in system performance and eliminates expensive mid-project corrections. Earth'smart powered by tect's Earth'smart™ program is built around that principle — one team covering architecture, engineering, and construction, with direct manufacturer input through the earth'smart powered by tectApp™ community of 70+ building product partners from concept through completion.

What Most Homeowners Get Wrong About Rebuild Costs

Three gaps show up repeatedly — and each one catches homeowners off guard at the worst possible moment.

The pre-construction bill arrives first. Debris removal, soil remediation, engineering, and permits routinely consume $100,000–$200,000 before construction starts. Most homeowners don't realize this until they've burned through their insurance advance.

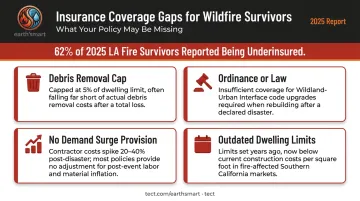

Insurance rarely covers the full picture. A United Policyholders 6-month survey of 2025 LA fire survivors found 62% reported being underinsured and 33% didn't yet know if they were. Common policy gaps include:

- Debris removal capped at 5% of the dwelling limit

- Insufficient or absent Ordinance or Law coverage for WUI code upgrades

- No demand surge provision as contractor costs spike post-disaster

- Dwelling limits set years ago, well below current construction costs

The time cost of rebuilding adds up fast. A 24-month rebuild at current LA-market temporary housing rates can add $60,000–$120,000 in out-of-pocket housing costs. Most homeowners never model this when reviewing their coverage limits at renewal.

How to Estimate Your Wildfire Rebuild Budget

Start with an independent cost assessment. An insurance adjuster's estimate is a starting point, not a final number. Independent construction cost estimators or architects experienced in California post-fire rebuilds — including current WUI code requirements and local labor pricing — will produce significantly more reliable figures.

Build your budget in phases, assigning a dollar range to each of the five phases above. Then add a 20–30% contingency buffer specifically for demand surge. That buffer reflects documented pricing behavior in California post-disaster markets, where contractor and materials costs routinely spike 20–40% within months of a major fire event.

Evaluate total cost of ownership, not just construction cost. A home built to a higher resilience standard may cost $15,000–$50,000 more today. Run a 10-year comparison:

- Potential insurance premium differences for lower-risk builds

- Reduced probability of another total loss

- Lower long-term maintenance costs from durable, non-combustible systems

- Possible financing and resale advantages

In most 10-year comparisons, the resilient build pays for its premium through insurance savings and avoided loss alone — and that's before factoring in the reduced likelihood of rebuilding a second time.

Frequently Asked Questions

What is the cost of rebuilding after a wildfire in California?

Total costs range from roughly $300,000 for smaller, simpler rebuilds to over $1 million for larger homes in high-severity zones. Pre-construction costs (debris removal, remediation, permits, engineering), WUI code compliance, and demand surge all push totals well above raw construction estimates. Budgeting for construction alone consistently falls short.

How is rebuilding going after the LA fires?

As of January 2026, approximately 2,600 residential permits had been issued and 3,340 were under review. That's roughly one permit for every five of the nearly 13,000 homes lost. Permitting has accelerated, but progress remains constrained by insurance reimbursement timelines, high material and labor costs, and ongoing financial strain on households.

What does debris removal cost after a California wildfire?

For homeowners enrolled in LA County's Phase II program through the Army Corps of Engineers, debris removal has no direct out-of-pocket cost, though insurance proceeds designated for debris removal must be assigned to avoid duplication of benefits. Private removal can be substantial — Camp Fire data suggests roughly $100,000 per parcel on average. Check your policy's debris removal coverage limit before assuming full coverage.

Does homeowners insurance cover the full cost of rebuilding after a wildfire?

Most standard policies fall short. Common gaps include:

- Dwelling limits set below current construction costs

- Debris removal capped at 5% of the dwelling limit

- Inadequate or absent Ordinance or Law coverage for WUI code upgrades

- No demand surge provision

A United Policyholders survey found 62% of 2025 LA fire survivors reported being underinsured. Six-figure out-of-pocket gaps are common even for insured homeowners.

How long does it take to rebuild a home after a wildfire in California?

Full rebuilds typically take 18–36 months from lot clearance to occupancy, depending on permitting speed, contractor availability, and project complexity. CDI's rule that survivors have at least 36 months to collect replacement cost after first payment reflects this timeline. The extended duration creates significant temporary housing cost exposure that most homeowners underestimate.

What is Chapter 7A and how does it affect rebuild costs?

Chapter 7A is now consolidated into California's WUI Code (Title 24, Part 7, effective January 1, 2026). It sets mandatory standards for homes in high fire hazard severity zones, covering ember-resistant vents, ignition-resistant siding, Class A roofing, and dual-pane tempered glazing. A 2025 Headwaters/IBHS model found these requirements added $13,070 to a 1,750 sq ft Altadena home. Ordinance or Law coverage on your homeowners policy is designed specifically to fund these required upgrades.

![Average Cost to Rebuild a House After Fire [2026 Data]](https://file-host.link/website/tect-preys7/assets/blog-images/bc6b2e3c-b712-4dea-8295-12d4e6042cca/1780066015511649_fc1207abcb7b4a2885f02468b763a4b9/1080.webp)