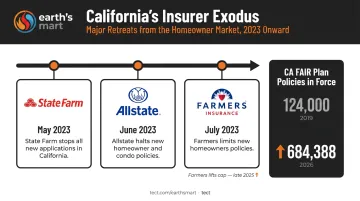

State Farm stopped accepting new California property applications in May 2023. Allstate and Farmers followed with restrictions. The result? The FAIR Plan has grown from roughly 124,000 policies in 2019 to 684,388 total policies in force as of March 2026, with $750 billion in total exposure.

This guide explains exactly what the FAIR Plan is, what it covers (and doesn't), what it costs, and how to use it as a bridge — not a permanent solution.

TL;DR: Key Things to Know About the California FAIR Plan

- The FAIR Plan is California's insurer of last resort — it covers basic fire perils only, not a full homeowners policy

- Core coverage: fire, lightning, smoke, and internal explosion; no liability, theft, or water damage by default

- Most policyholders need a separate Difference in Conditions (DIC) policy to fill what the FAIR Plan leaves out

- Rates are rising — the FAIR Plan filed for a 35.8% average rate increase in October 2025

- Treat it as temporary: documented home hardening — fire-resistant materials, defensible space, ember-resistant vents — gives insurers a reason to take you back

What Is the California FAIR Plan — and Why Are Record Numbers of Homeowners on It?

The Basics

FAIR stands for Fair Access to Insurance Requirements. Established in 1968, it's a state-mandated insurance pool that guarantees basic fire coverage to property owners denied by private insurers. Two things homeowners often get wrong:

- It is not a government agency

- It is not funded by taxpayers

All private insurers licensed to operate in California back the FAIR Plan financially, sharing risk in proportion to their market share.

The Private Market Pullback

The FAIR Plan's explosive growth is a direct result of major insurers retreating from California:

- State Farm stopped accepting new California property applications on May 27, 2023, then announced non-renewals of approximately 30,000 personal lines policies in March 2024

- Allstate stopped writing new homeowner and condo policies in California, reported in June 2023

- Farmers limited new homeowners policies in July 2023 (though it lifted that cap in late 2025)

For homeowners in high-fire-risk ZIP codes, this left the FAIR Plan as the only available option.

The January 2025 LA Wildfires: A System Under Pressure

According to CDI Bulletin 2025-4, as of February 11, 2025, the FAIR Plan had received 4,794 claims from the Palisades and Eaton fires combined, with estimated losses of approximately $4 billion.

To cover those losses, the Commissioner approved a $1 billion assessment on member insurers.

Here's why that matters even if you have private insurance: member insurers may recoup up to 50% of that assessment through temporary surcharges on their own policyholders. It's a regulated process, not automatic — but FAIR Plan losses ripple outward across the entire California market.

California's Response: The Sustainable Insurance Strategy

Those losses accelerated pressure on Sacramento to stabilize the market. The state's answer is the Sustainable Insurance Strategy (SIS). Under SIS, insurers must commit to writing at least 85% of their statewide market share in wildfire-distressed areas, while gaining the ability to use forward-looking catastrophe models and include California-only reinsurance costs in rate filings. In April 2026, Travelers announced expanded California homeowners availability under SIS — the first major insurer to publicly expand coverage under the new framework. Whether others follow will determine how quickly homeowners in high-risk areas regain real options.

What the California FAIR Plan Covers — and Its Critical Gaps

A standard FAIR Plan dwelling policy is a named-perils policy — it only covers what is explicitly listed. Unlike a standard HO-3 policy, which covers your dwelling on an open-perils basis, the FAIR Plan pays only for damage caused by perils specifically named in the policy. The four core perils are:

- Fire and lightning

- Smoke

- Internal explosion

- Windstorm and hail (when added via extended coverage endorsement)

Coverage applies to the physical structure up to $3 million per residential property. If the peril isn't named, it isn't covered.

Optional Add-Ons and ACV vs. RCV

You can expand FAIR Plan coverage through endorsements:

- Windstorm and hail (extended coverage)

- Vandalism and malicious mischief

- Dwelling replacement cost value (RCV) — critical; see below

- Personal property replacement cost

- Fair rental value

- Ordinance or law coverage

- Debris removal

One endorsement stands above the rest: Replacement Cost Value (RCV). The FAIR Plan defaults to Actual Cash Value (ACV), meaning depreciation is applied before your claim is paid. For a 20-year-old home, the gap between what you receive and what it costs to rebuild can be enormous. RCV pays the actual cost to repair or replace — and most mortgage lenders require it. If you're on the FAIR Plan, upgrading to RCV is one of the most consequential coverage decisions you'll make.

What the FAIR Plan Does NOT Cover

These exclusions catch homeowners off guard:

- Personal liability — if someone is injured on your property, you have no protection

- Additional living expenses (Fair Rental Value is optional and limited — not the same as full ALE)

- Theft

- Water damage from burst pipes or appliances

- Flooding and earthquakes

- Falling objects

Taken together, these gaps represent significant financial exposure. That's where a DIC policy comes in.

Why a DIC Policy Is Essential

A Difference in Conditions (DIC) policy is a supplemental policy designed to wrap around the FAIR Plan and fill those gaps.

DIC policies typically cover:

- Theft and water damage

- Personal liability

- Additional living expenses

- Optionally, earthquake and flood

The FAIR Plan doesn't sell DIC policies directly, but the California Department of Insurance maintains a list of DIC providers. A licensed broker can help you source and compare options. A FAIR Plan + DIC combination approximates an HO-3 policy — but typically costs more and requires managing two separate policies.

How Much Does the California FAIR Plan Cost?

What We Know About Current Premiums

No current official statewide average FAIR Plan residential premium exists in public sources. The most-cited figure is approximately $3,200 per year, drawn from a 2022 FAIR Plan spokesperson quote. Given significant rate increases since then, treat it as a floor, not a current benchmark.

For context on what you're paying relative to coverage: FAIR Plan policyholders typically pay more than private market rates for a narrower policy, then add DIC costs on top.

What Drives Your Premium

Key rating factors include:

- Location: proximity to brush, wildland, and fire-hazard severity zone designation

- Construction type: roof material, siding, and foundation

- Home age and overall condition

- Coverage amount and deductible level

- Endorsements added (RCV, vandalism, fair rental value, etc.)

Homes in extreme fire-hazard severity zones will carry higher base premiums than those in lower-risk areas.

The Rate Trajectory

According to AM Best and the Los Angeles Times, in October 2025, the FAIR Plan filed for a 35.8% average rate increase for personal dwelling fire policies. CDI is reviewing the filing; new rates are expected around April 2026. Wildfire-prone areas would see larger increases; lower-risk areas may actually see decreases.

Reducing Your Premium

The FAIR Plan offers verified mitigation discounts for documented home-hardening measures, including:

- Class A fire-rated roof

- Cleared vegetation and debris within the ember-resistant zone (0–5 feet)

- Defensible-space compliance (Zones 1 and 2 per CAL FIRE standards)

- Ember and fire-resistant vents

- Double-paned windows or shutters

- Noncombustible bottom 6 inches of exterior walls

- Enclosed eaves

A broker can verify which measures qualify for your property and calculate the discount impact — including whether a higher deductible makes sense for your situation.

Who Qualifies for the California FAIR Plan and How to Apply

Eligibility Requirements

The FAIR Plan is available to California residents and businesses who cannot obtain coverage in the standard market. Core eligibility criteria:

- California property that meets basic building code and maintenance standards

- Proof of denied or non-renewed coverage from private market insurers, showing you made a genuine attempt to obtain standard coverage

- Property must not be vacant or unoccupied for more than one year (unless under active construction), used for illegal activity, or intended for demolition

Coverage is available for single-family homes, condos, townhomes, rental properties, and seasonal homes — not just owner-occupied primary residences.

The Application Process

- Connect with a registered FAIR Plan broker — not all licensed agents are registered with the FAIR Plan; confirm before engaging. There is no additional broker fee for FAIR Plan applications.

- Broker conducts a private market search on your behalf — documenting that standard coverage is unavailable to you

- Submit application with home details and property information; current exterior photos are required when combined coverage limits exceed $1,500,000

- Undergo a home inspection if required by the FAIR Plan

- Receive a quote, select endorsements, and pay the first premium to activate coverage

You can contact the FAIR Plan directly, but a registered broker handles the private market search and paperwork on your behalf — making that the faster, simpler route for most homeowners.

Using the FAIR Plan as a Bridge: How to Return to the Private Market

The FAIR Plan is explicitly designed as a temporary solution. Treating it as a permanent arrangement means accepting narrower coverage, higher combined costs (FAIR Plan + DIC), and exposure to assessment surcharges. The goal is to document your way back to private market eligibility.

Home Hardening: Your Most Powerful Lever

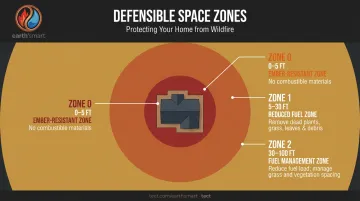

CAL FIRE's defensible space standards define the baseline:

- Zone 0 (0–5 feet): Ember-resistant zone — no combustible materials directly adjacent to the structure

- Zone 1 (5–30 feet): Remove dead plants, grass, leaves, and combustible debris

- Zone 2 (30–100 feet): Reduce fuel load, manage grass height and vegetation spacing

Beyond defensible space, the construction decisions you make during a rebuild determine your long-term insurability. For homeowners in Pacific Palisades and the Eaton corridor rebuilding after the 2025 fires, this is the moment to build differently.

Earth'smart powered by tect, a Southern California architecture, engineering, and construction firm specializing in WUI rebuilds, approaches post-fire reconstruction through its Earth'smart™ program. Rebuilding to minimum code is no longer sufficient for today's insurance environment. Earth'smart powered by tect designs homes with fire-resistive exterior wall systems using pre-insulated concrete masonry, non-combustible assemblies throughout, Class A roofing systems, and integrated on-site fire suppression — including a vapor dome system with dedicated water supply for fire events.

The firm works across two paths: turnkey delivery (full team from concept through construction) and an advisory path for homeowners with existing teams. Both draw on the earth'smart powered by tectApp™ community of 70+ building product manufacturers to ensure system-level coordination from the start.

The practical insurance implication: homes built with these assemblies are better positioned for private market underwriting, because they address risk at the system level rather than just satisfying permit minimums.

That mitigation work only helps if you can prove it. Keep a file with invoices, photos, permits, material labels, and inspection records for every measure you take. This documentation supports FAIR Plan discount applications, DIC underwriting, and private market re-entry conversations with your broker.

Keep Shopping the Private Market

The Sustainable Insurance Strategy (SIS) is shifting carrier appetite, slowly. Recent moves signal the market is starting to open in specific areas:

- Travelers expanded California homeowners availability in April 2026 under SIS commitments

- Farmers lifted its cap on new policies in late 2025

The market won't open uniformly — but specific ZIP codes may become accessible again as carriers fulfill SIS writing requirements.

A registered broker can monitor availability in your ZIP code and move you off the FAIR Plan when a qualifying policy becomes available. Don't wait for carriers to find you.

Frequently Asked Questions

What is the average cost for a California FAIR Plan?

The most recent publicly cited figure is approximately $3,200 per year (2022 FAIR Plan spokesperson), though current premiums are quote-specific and likely higher following the 2025 wildfires. Most policyholders also carry a separate DIC policy, making the combined cost higher than a standard private homeowners policy — for less comprehensive coverage.

What does the California FAIR Plan cover?

The FAIR Plan covers four named perils: fire and lightning, smoke, and internal explosion. Personal liability, water damage, theft, and additional living expenses are not included in the base policy. Some gaps can be addressed through optional endorsements; others require a separate DIC policy.

Is the California FAIR Plan good insurance?

The FAIR Plan provides critical fire coverage when no private market option exists and typically satisfies mortgage lender requirements. It is not a substitute for a comprehensive HO-3 policy, which is why pairing it with a DIC policy — and treating it as a temporary measure — is the standard recommendation.

Do I need a DIC policy with the California FAIR Plan?

Most homeowners on the FAIR Plan need one. A DIC policy fills the major coverage gaps — particularly personal liability, theft, and water damage — that the FAIR Plan leaves exposed. A licensed broker can help you compare DIC options from the CDI's list of providers.

How can I lower my California FAIR Plan premium?

Document and submit verified home-hardening improvements — Class A roofing, defensible space compliance, ember-resistant vents, double-paned windows, and enclosed eaves are among the qualifying measures. Choosing a higher deductible also reduces your premium. Work with your broker to identify which measures apply to your specific property.

Can the California FAIR Plan drop me?

Yes, for specific reasons: non-payment of premium, vacancy beyond one year, property slated for demolition, or property connected to illegal activity. Non-renewal notices must generally be issued at least 30 days in advance.