![Average Cost to Rebuild a House After Fire [2026 Data]](https://file-host.link/website/tect-preys7/assets/refined-images/1780579704434000_b10b362667074dc283d3d9f70a1ab290/360.webp)

That scale turned rebuilding from a personal project into a regional capacity crisis — one where contractors, permits, materials, and inspectors are all competing across thousands of loss sites simultaneously.

Before going further, one distinction matters: fire damage restoration means repairing salvageable structure — smoke remediation, partial repairs, structural patching. A full rebuild is ground-up reconstruction after a total loss. These carry dramatically different price tags, timelines, and decisions. This article focuses on full rebuilds.

What follows covers current cost ranges by tier, the factors that push those numbers up or down, a complete breakdown of what you're actually paying for, and the decisions that determine whether a rebuilt home lasts 30 years — or a hundred.

Key Takeaways

- Full rebuilds run $150–$250/sf nationally; LA wildfire zones report $450–$800+/sf based on local estimates

- Five factors drive final cost: home size, demolition scope, WUI code requirements, material choices, and post-disaster labor shortages

- 69% of total-loss homeowners in the LA fires lacked enough insurance to rebuild, with an average underinsurance gap of $247/sf

- Building to wildfire-resilient standards costs more upfront, but typically less than a second rebuild after another loss

How Much Does It Cost to Rebuild a House After Fire? [2026 Overview]

There is no single fixed number. Rebuild costs shift based on location, damage scope, material choices, and local market conditions — and in post-wildfire zones, demand spikes can compress contractor availability while driving rates sharply upward.

Before comparing per-square-foot figures, check one thing: your insurance policy's replacement value was likely calculated years ago. It may not reflect 2026 material costs, mandatory code upgrades, or post-disaster labor premiums.

Basic Rebuild (Standard Replacement)

What's included: Standard-grade materials, code-minimum construction, like-for-like replacement of the original footprint and layout.

Typical cost range: $150–$200/sf nationally for non-disaster markets.

Best for: Homeowners with limited coverage in lower-risk areas where WUI fire code upgrades aren't mandatory and post-disaster demand hasn't distorted local labor markets.

Mid-Range Rebuild (Updated Materials, Improved Systems)

What's included: Upgraded finishes, modern electrical and plumbing, improved insulation and building envelope performance. Includes some fire-resilient material choices without a full WUI-compliant specification package.

Typical cost range: $200–$350/sf nationally; higher in California markets.

Best for: Homeowners with solid coverage who want meaningful improvements over their previous home without committing to a full premium build.

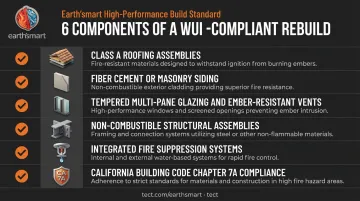

High-End / Resilient Rebuild (WUI-Compliant, Long-Term Performance)

What's included:

- Fire-resistant roofing (Class A assemblies)

- Fiber cement or masonry siding

- Tempered or multi-pane glazing and ember-resistant vents

- Non-combustible structural assemblies

- Integrated fire suppression systems

- Full California Building Code Chapter 7A compliance, plus beyond-code upgrades where warranted

Typical cost range: $450–$650/sf in LA wildfire areas per IBHS estimates; homeowner-reported bids in the Palisades area have reached $800/sf.

Best for: Homeowners in WUI zones — Pacific Palisades, Altadena, and similar high-risk communities — who need a home engineered to perform in future events, not just survive the permitting process.

Key Factors That Affect the Cost to Rebuild

Rebuilding after a fire isn't priced like new construction. Post-disaster conditions introduce cost layers that most homeowners don't see coming: contractor shortages, compressed supply chains, code enforcement backlogs, and mandatory site remediation — all of which hit before a single wall goes up.

Extent of Damage and Demolition Scope

Even before construction begins, clearing the site is a significant expense. Private demolition and debris removal for a fire-damaged home can run $10,000–$50,000+ depending on home size, hazardous material content, and local disposal requirements.

LA County offered a government-managed debris removal program for Palisades and Eaton fire survivors ; insured owners who opted in were required to assign their insurance proceeds designated for debris removal to offset public costs. By May 2025, CalOES reported 5,000+ properties cleared through Phase 2, removing over 2 million tons of debris.

LA County Public Health also flagged that wildfire ash may contain heavy metals, lead, and asbestos. Soil testing is often required before permits can be issued, adding both cost and schedule delay.

Home Size and Configuration

Total square footage scales every cost category linearly: labor, materials, inspections, and systems all grow with the footprint. But configuration matters just as much.

Multi-story homes, irregular floor plans, and long open spans cost considerably more per square foot than a simple rectangular single-story. A complex hillside home in Pacific Palisades carries a fundamentally different cost profile than a flat-lot ranch house of identical square footage.

Location and Local Building Codes

Homes in WUI zones face mandatory fire-resistant construction requirements under California Building Code Chapter 7A, covering roofing assemblies, exterior wall systems, vents, windows, and deck surfaces. IBHS estimated that meeting these requirements adds approximately $13,070 to the cost of a 1,750-square-foot home over standard construction.

For context: California and Colorado are currently the only Western states with mandatory wildfire codes in effect statewide. Homeowners rebuilding in mapped WUI zones cannot opt out of these requirements, and inspectors in post-disaster zones are enforcing them closely.

Labor costs compound this. Verisk reported residential retail labor costs up 5.3% from January 2024 to January 2025, with concrete mason labor up 26.3% over that same period. Those are national figures. LA-specific costs run higher.

Material Selection and Fire-Resistant Upgrades

Fire-resistant materials carry a real cost premium over standard wood-frame construction:

- Fiber cement siding vs. wood or vinyl

- Class A roofing assemblies (metal, tile, or rated composites) vs. standard asphalt shingles

- Tempered or multi-pane glazing vs. single-pane windows

- Ember-resistant vents vs. standard mesh vents

- Concrete masonry or non-combustible assemblies vs. standard framing

IBHS found that going beyond code minimums to meet IBHS Wildfire Prepared Home Plus standards adds roughly 3% over a $500,000 traditional build. For the risk reduction and insurability benefits that follow, that's a manageable tradeoff.

California's Department of Insurance has required insurers to provide discounts for Safer from Wildfires actions, which means resilient material choices can reduce ongoing insurance premiums, though the exact discount varies by insurer and policy.

Labor Availability and Contractor Quality

In the aftermath of a major wildfire, contractor demand far outpaces supply. NAHB and HBI estimated the skilled labor shortage caused $10.8 billion in annual economic impact nationally, with an average 1.98-month delay per project. That's under normal market conditions.

In post-wildfire zones, homeowners who wait to engage a contractor can face a 6–18 month queue just to begin construction.

The California Contractors State License Board issued a January 2025 consumer alert urging wildfire survivors to verify contractor licenses before signing contracts. Unlicensed bids that look cheaper often become permit failures or insurance disputes.

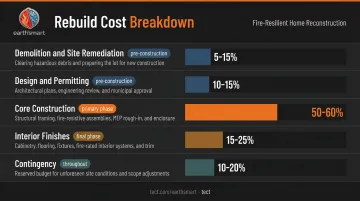

Full Rebuild Cost Breakdown: What You're Actually Paying For

Most homeowners budget for the construction phase and miss several significant cost categories that arrive before and during it. Here's what a full rebuild actually costs:

| Cost Category | Timing | Typical Share of Total |

|---|---|---|

| Demolition, debris removal, site remediation | One-time, pre-construction | 5–15% of total |

| Design, engineering, permitting, fees | One-time, pre-construction | 10–15% of total |

| Core construction (structure, envelope, systems) | One-time, primary phase | 50–60% of total |

| Interior finishes and fixtures | One-time, final phase | 15–25% of total |

| Contingency and hidden costs | Throughout project | 10–20% added buffer |

Demolition and site remediation covers teardown, hauling, hazardous material disposal, lot clearing, and any soil or environmental testing required before permits can be issued. In wildfire zones, this is rarely simple.

Design, engineering, and permitting includes architect fees, structural engineering, permit applications, plan check fees, HOA approvals, and inspections. CalMatters reported that by January 2026, local governments had issued 2,600+ residential permits — roughly one permit for every five homes lost. Approvals have accelerated, but permitting still adds weeks to schedules and thousands in fees — especially on hillside and WUI sites where plan check requirements are more stringent.

Core construction — foundation through roofing, all systems — is where material tier choices have the biggest dollar impact. Changing structural or systems decisions after framing starts can add $20,000–$50,000+ in rework costs.

Interior finishes are highly variable. The difference between a standard and premium finish package can swing total project cost by $75–$150/sf or more.

Contingency should be a dedicated line item — budget 10–20% of total project cost. This covers code-required upgrades discovered during permitting, unexpected soil conditions, utility reconnection delays, and temporary housing costs. Full rebuilds typically run 12–24+ months, so carrying costs add up.

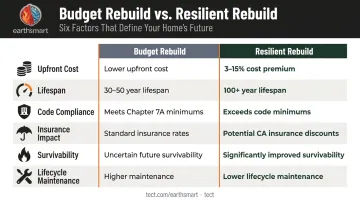

Budget Rebuild vs. Resilient Rebuild: What's the Real Difference?

Every post-fire homeowner faces the same core decision: rebuild to the same standard as before, or build to a higher performance level. For homeowners in WUI zones, that decision has consequences that outlast the construction budget.

| Factor | Budget Rebuild | Resilient Rebuild |

|---|---|---|

| Upfront cost | Lower | Higher (roughly 3–15% premium over code-minimum) |

| Expected lifespan | 30–50 years (standard construction) | 100+ years (engineered systems, durable materials) |

| WUI code compliance | Meets Chapter 7A minimums | Meets and exceeds minimums |

| Insurance premium impact | Standard rates | Potential discounts under CA Safer from Wildfires program |

| Future event survivability | Uncertain | Significantly improved |

| Long-term maintenance | Higher (more frequent replacement cycles) | Lower (durable assemblies reduce lifecycle costs) |

IBHS research shows resilience premiums are smaller than most homeowners assume. Going from code-minimum to IBHS Wildfire Prepared Home Plus adds roughly 3% to a $500,000 build. Meanwhile, the average underinsurance gap facing LA wildfire victims is $247/sf — a shortfall that trimming ember-resistant vents won't close.

A resilient rebuild also isn't just about materials. It requires early coordination between architect, structural engineer, and product manufacturers. When those decisions happen in sequence — design first, materials later, systems last — conflicts surface during construction that are expensive to resolve and often recreate the same vulnerabilities as the original home.

That coordination problem is what earth'smart powered by tect is built around. Through the earth'smart powered by tectApp community of 70+ building product manufacturers, the right technical expertise is brought in during design, not after framing starts. Systems are specified and integrated from concept through construction — which is how you get a home engineered to last 100+ years, not just pass inspection.

What Most People Get Wrong When Budgeting a Fire Rebuild

Focusing only on per-square-foot construction cost. Pre-construction costs (demolition, design, permits) and carrying costs (temporary housing, utility reconnection, landscaping) can collectively add 25–40% to the stated build cost. A $600/sf construction bid on a 2,000-square-foot home is a $1.2M construction cost — not a $1.2M total project cost.

Assuming insurance covers the gap. United Policyholders' one-year LA fire survey found that 69% of total-loss respondents didn't have enough insurance to rebuild, with an average shortfall of $247/sf. Two-thirds of Palisades fire victims and 82% of Eaton fire victims were uncertain they had enough resources to cover costs not paid by insurance.

Most policies set replacement values years ago — before material costs escalated, before mandatory code upgrades, and before post-disaster labor premiums became standard. Price the actual rebuild first; then reconcile it against your coverage.

Treating the rebuild as a replacement. For homeowners in fire-prone areas, rebuilding the same home with the same materials means facing the same outcome in the next event. Earth'smart powered by tect's position is direct: a rebuild is the opportunity to ensure the home performs differently — with fire-resistive assemblies, non-combustible materials, and integrated systems decided correctly from the start. That requires a coordinated team making the right calls early, not a fragmented process that delivers a home that looks complete but fails structurally when it counts.

Frequently Asked Questions

How much does it cost to rebuild a house after a fire?

A full rebuild (ground-up reconstruction) runs $150–$250/sf in most national markets. In LA wildfire zones, local estimates from IBHS and homeowner bids range from $450 to $800+/sf. A 2,000 sq. ft. home in Pacific Palisades or Altadena could realistically cost $1M–$1.6M+ for construction alone, before pre-construction and contingency costs.

How much does it cost to build a 2,000 square foot house in 2025?

Nationally, a 2,000 sq. ft. new build runs roughly $300,000–$500,000 in typical markets. In California, expect $600,000–$1.2M+. In post-wildfire demand zones like the Palisades or Altadena, WUI code compliance and post-disaster labor premiums routinely push totals above $1.2M for a mid-size home.

Is $300,000 enough to build a house?

In lower-cost national markets, $300,000 may cover a basic new build. In Southern California wildfire zones, it falls well short. A mid-size home in Pacific Palisades or Altadena typically runs $700,000–$1.5M+ for construction , not counting demolition, design, permitting, or interior finishes.

Does homeowners insurance cover the full cost to rebuild after a fire?

Most standard policies cover a portion of rebuild costs, but replacement value estimates are often years out of date. Rising material costs, post-wildfire labor premiums, and mandatory code upgrade requirements have created significant gaps: United Policyholders found the average LA fire underinsurance gap was $247/sf. Review your policy limits against current rebuild costs before your project starts.

What is the difference between fire damage restoration and rebuilding a house?

Restoration involves repairing salvageable structure : smoke and soot remediation, water damage repair, partial structural patching. A rebuild is ground-up reconstruction after a total loss. Wildfires, particularly in WUI zones, typically produce total losses that require full rebuilds rather than restoration.

How long does it take to rebuild a house after a fire?

A full rebuild typically takes 12–24+ months from demolition to move-in, covering debris clearance, permitting, design, contractor scheduling, inspections, and utility reconnection. In post-wildfire zones, where local permitting capacity is stretched thin, timelines consistently run toward the 24-month end.