Introduction

Most commercial property owners assume their building is properly insured. Many are wrong.

The gap between what an owner thinks they're covered for and what an insurer will actually pay often comes down to one thing: an inaccurate valuation.

Commercial building valuation for insurance is the process of determining the cost to rebuild or replace a structure from the ground up. That figure — not market value or the tax assessment — is what sets your coverage limits.

This guide is for commercial property owners, real estate investors, and anyone rebuilding or insuring a high-value structure.

If your coverage limit is based on a purchase price, an outdated appraisal, or a number pulled from an online calculator, you may be carrying far less protection than you think — and you won't find out until a claim.

Key Takeaways

- Insurance valuation measures replacement cost — what it costs to rebuild your home — not what it would sell for on the market

- The three main valuation methods are Replacement Cost Value (RCV), Actual Cash Value (ACV), and Functional Replacement Cost — and the difference between them determines your actual payout at claim time

- Underinsurance is common: many US homeowners discover their coverage falls short only after a loss, when rebuilding costs have already climbed beyond their policy limits

- Key valuation drivers include construction type, square footage, materials, local labor rates, code compliance upgrades, and site access conditions

- Valuations go stale — wildfire rebuilds, code changes, and rising construction costs can push the real number well above what your policy reflects

What Is Commercial Building Valuation for Insurance?

Commercial building valuation for insurance is the process of calculating what it would cost to rebuild a structure from the ground up using comparable materials and current construction standards. That figure — the replacement cost — is what determines your coverage limit, not what the building is worth on the open market.

Three Numbers That Get Confused

These three figures measure entirely different things:

- Replacement cost — the cost to reconstruct the building using similar materials at today's prices; this is what insurance covers

- Market value — what a willing buyer would pay, which includes land value and fluctuates with real estate conditions

- Assessed/tax value — a government-assigned figure for taxation purposes, often well below both of the above

As RICS notes in its reinstatement cost assessment standard, the declared value for insurance purposes has no direct relationship to market value. Using market value or a tax assessment to set coverage limits is a costly mistake. In high-demand markets, a building can be worth far more than it costs to rebuild — meaning you'd pay premiums on inflated coverage. In distressed markets, the reverse applies: the building might cost more to replace than it would sell for.

Why Commercial Valuations Are More Complex Than Residential

Commercial buildings are not just larger houses. They involve a different order of complexity than residential structures:

- Specialized mechanical, electrical, and plumbing (MEP) systems

- Multiple occupancy classifications with distinct fire and life safety requirements

- Fire suppression infrastructure that must meet code before occupancy

- Code compliance across more regulatory bodies than residential projects

- Mandatory professional fees — architect, structural engineer, permits, project management — required before construction begins

A valuation that misses any of these line items can leave a gap of hundreds of thousands of dollars between your coverage limit and your actual rebuild cost.

Why Accurate Commercial Building Valuation Is Critical

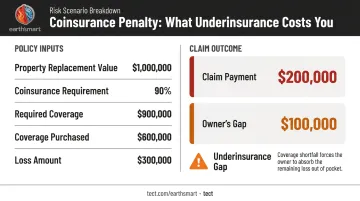

The Coinsurance Penalty

Most commercial property policies include a coinsurance clause requiring the insured to carry coverage equal to a minimum percentage of the property's actual replacement cost — commonly 80%, 90%, or 100%, as described by IRMI. If coverage falls short of that threshold, the insurer reduces claim payouts proportionally.

Travelers' coinsurance example illustrates this clearly:

| Scenario | Figure |

|---|---|

| Property replacement value | $1,000,000 |

| Coinsurance requirement | 90% |

| Required coverage | $900,000 |

| Coverage actually purchased | $600,000 |

| Loss amount | $300,000 |

| Claim payment (before deductible) | $200,000 |

The owner absorbs $100,000 of a $300,000 loss — not because the policy excluded anything, but because the building was underinsured. In a total loss, the shortfall scales accordingly.

Insurability, Premiums, and Rebuild Viability

Accurate valuation isn't only about what happens at claim time. It affects:

- Whether a property is insurable at all, particularly in high-risk zones

- How premiums are calculated (under- and over-insurance both create problems)

- Whether the rebuild budget is actually sufficient to complete reconstruction

In wildfire zones, flood plains, and earthquake-prone regions, rebuild costs are often elevated and construction timelines stretch longer than standard markets. Buildings engineered to higher resilience and fire-resistance standards can affect how insurers assess the property and its risk profile.

That connection between construction quality and insurance costs is increasingly measurable. FM, a major commercial property insurer, announced a US$400 million resilience credit in 2024, structured as a 5% premium offset for eligible policies — demonstrating that how a building is built directly affects what owners pay to insure it.

How Commercial Building Insurance Valuation Works

A complete commercial valuation is not a single number pulled from a database. It is a structured process that accounts for every cost component required to fully rebuild — from site preparation through final finishes, including professional fees and regulatory compliance.

Qualified appraisers base valuations on current construction costs at the time of assessment. This is why figures become outdated and why periodic review is non-negotiable.

Two main delivery approaches exist:

- Desktop assessments — use data inputs, cost indices, and building characteristics to generate an estimate without a site visit; appropriate for straightforward structures or initial screening

- Onsite/physical appraisals — a qualified professional visits the property; necessary for complex or high-value buildings where physical characteristics meaningfully affect cost

Step 1: Identify the Building's Physical Characteristics

The foundational data inputs that drive every downstream calculation:

- Gross floor area and number of stories

- Construction type (steel frame, reinforced concrete, masonry, wood frame)

- Year built and current condition

- Interior finish quality

- Specialized features: built-in equipment, HVAC systems, elevators, fire suppression

Errors or omissions here propagate through the entire estimate. If the square footage is wrong or a major system is overlooked, the final figure will be wrong — and there's no methodology fix for a bad input.

Step 2: Calculate Core Construction and Site Costs

Primary cost components in a rebuild estimate:

- Structural construction: materials and labor

- Interior finishes and fit-out

- Mechanical, electrical, and plumbing systems

- Demolition and site clearance — frequently underestimated

- External site features: parking areas, fencing, access infrastructure

Site-specific costs matter more than most line items. Demolition and debris removal are real expenses that online calculators and generic estimates routinely omit. Aon's research shows that some replacement-cost appraisals include only a 7% debris-removal allowance, which may be wholly inadequate for the specific property. The RICS example for a high-specification office applies demolition costs at 15% of rebuilding cost — a figure that illustrates how material these line items can be.

Step 3: Add Professional Fees, Code Compliance, and Rebuild Timeline

The "soft costs" that are legally required for any rebuild:

- Architect and structural engineering fees

- Permits and regulatory approvals

- Project management

- Compliance with current building codes — not the codes in effect when the building was originally constructed

Code compliance is a common blind spot. A building that was fully code-compliant when built may require significant upgrades to current fire safety, energy efficiency, accessibility, or structural standards when rebuilt. Standard replacement-cost policies typically exclude these code-upgrade costs; separate ordinance or law coverage addresses this gap.

The rebuild timeline flows directly from this same process. A longer rebuild period determines how much Business Interruption or loss-of-rent coverage is needed — underestimate it, and income protection runs out before the building is operational.

Key Factors That Affect Commercial Building Insurance Valuation

Construction Type and Materials

ISO construction class is the foundational variable. Steel frame and reinforced concrete carry different per-square-foot rebuild costs than wood frame or masonry. Specialty materials, historic finishes, and custom architectural elements can push replacement costs significantly above generic estimates — a standard cost calculator won't capture a hand-laid terra cotta facade or a custom curtain wall system.

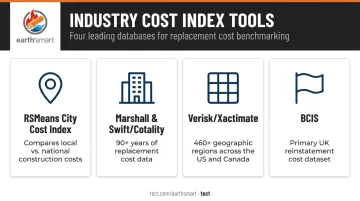

Geographic Location and Local Cost Conditions

Location creates meaningful variation that generic estimates miss entirely. Labor availability, regional material costs, transportation logistics, and local market conditions all shift the rebuild number. Tools used by adjusters and appraisers to account for this include:

- RSMeans City Cost Index — compares local project costs against the national average

- Marshall & Swift (Cotality) — over 90 years of replacement-cost data for commercial, industrial, and agricultural properties

- Verisk/Xactimate — pricing data across more than 460 geographic regions in the US and Canada

- BCIS — the primary UK reinstatement cost dataset

RLB's Q4 2024 North America Construction Cost Report shows national average costs rose 4.69% year-over-year, with Boston, Chicago, and Seattle tracking above that mark — a clear case for location-adjusted figures over national averages.

Building Code and Regulatory Compliance

Buildings must be rebuilt to current code, not the code in effect at original construction. Changes to fire safety, energy efficiency, accessibility, and structural standards accumulate over a building's lifetime. For older structures, the gap between original construction cost and current code-compliant rebuild cost can be substantial — and most standard replacement-cost estimates don't capture it.

Age, Condition, and Prior Renovations

Any improvements made since original construction must be reflected in the valuation. Owners who add a floor, upgrade HVAC, or complete a major renovation without updating their coverage limit are underinsured from day one.

Several factors compound this gap over time:

- Renovations and additions that increased square footage or system complexity

- Aging mechanical, electrical, and plumbing systems priced at current replacement costs

- Deferred maintenance that affects the scope of a full rebuild

- Changes in construction labor costs since the last appraisal

Occupancy Type and Use

Office, retail, industrial, multi-family, medical, and food service buildings each carry different code requirements, system complexities, and fit-out costs. A medical facility requires specialized plumbing, ventilation, and electrical systems that a warehouse does not. Using a generic commercial category instead of the actual occupancy type routinely produces underestimates — sometimes by 20–30% for specialized facilities.

Common Mistakes in Commercial Building Valuation

Using Market Value or Purchase Price as a Proxy

This is the most widespread error. Cotality explains that market value is the price agreed by a willing buyer and seller, while replacement cost is the estimated cost to construct a building of equal quality at current prices. These two figures can diverge by a wide margin. In high-demand markets, a building may sell for far more than it would cost to replace; in distressed markets, the reverse can be true. Neither case tells you what it costs to rebuild.

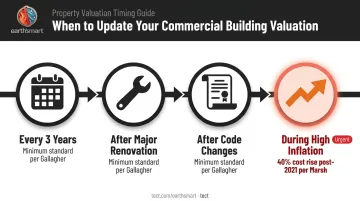

Treating Valuation as a One-Time Exercise

Construction costs, labor rates, building codes, and the property itself all change. Gallagher's guidance recommends a major review and reassessment at minimum every three years. Marsh's 2024 Property Valuation US Market Update noted that after several years of elevated inflation, equipment and construction costs had risen by roughly 40%. A valuation accurate in 2021 could represent a severe coverage shortfall today.

Underestimating Soft Costs and Site-Specific Expenses

Many owners — and some estimating tools — focus only on the structural shell and miss the full cost stack:

- Architect and engineering fees

- Demolition and debris removal

- Permit and regulatory compliance

- Code upgrades (often excluded from standard estimates)

- Rebuild timeline and its implications for income protection coverage

These omissions consistently produce underinsurance. A professional appraisal using real site data and current cost indices — not a generic online calculator — closes this gap more reliably than any shortcut.

Frequently Asked Questions

How do you determine the value of a building for insurance purposes?

Insurance value is determined by calculating replacement cost — what it would cost to rebuild using similar materials and current construction standards. This is typically done through a professional appraisal, a structured cost estimation tool, or a desktop assessment using detailed building data inputs.

What are the main types of building valuations used for insurance?

Three methods cover most commercial policies:

- Replacement Cost Value (RCV) — full rebuild cost, no depreciation deducted

- Actual Cash Value (ACV) — rebuild cost minus depreciation

- Functional Replacement Cost — applies when the rebuilt structure would differ materially from the original in type or construction

What is building valuation for insurance purposes?

It is the process of establishing what it would cost to rebuild a structure at the time of a loss. That figure sets the coverage limit, shapes your premium, and determines what a claim actually pays out.

What is the difference between replacement cost value and actual cash value for commercial buildings?

RCV covers the full cost to rebuild without depreciation deducted. ACV deducts depreciation, meaning the insurer pays considerably less — particularly on older or heavily depreciated structures. On a major loss, that out-of-pocket gap can run into hundreds of thousands of dollars.

How often should commercial building insurance valuations be updated?

At minimum every three years, per Gallagher's guidance — sooner after major renovations, code changes, or sharp construction cost shifts. During periods of elevated inflation, annual reviews are worth scheduling.

What happens if a commercial building is underinsured?

Most commercial policies include a coinsurance clause that reduces claim payouts proportionally when coverage falls below a required percentage of replacement cost. The shortfall is borne by the property owner — in a total loss, that can be financially devastating.