This guide covers what you need to know about your policy, how to file your claim correctly, the buy vs. rebuild decision under California law, and how to approach a rebuild as a permanent upgrade rather than a replica of what was lost.

Key Takeaways

- Your policy type (ACV, RCV, or Extended Replacement Cost) determines how much you can actually recover. Know the difference before the adjuster arrives.

- California insurers must acknowledge your claim within 15 calendar days and accept or deny within 40 days after proof of claim.

- According to RAND research on California wildfire survivors, 64% reported insufficient coverage to rebuild — underinsurance is the norm, not the exception.

- California law (Insurance Code 2051.5) gives you the right to use your insurance proceeds to buy a replacement home instead of rebuilding.

- A post-fire rebuild in a WUI zone is an opportunity to construct a home engineered to perform for 100+ years.

Understanding Your Fire Insurance Policy

The Three Coverage Types

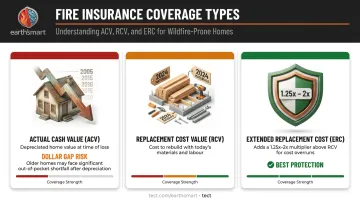

The gap between what your policy pays and what rebuilding actually costs typically hinges on one term on your declarations page.

- Actual Cash Value (ACV): Pays the depreciated value of your home — what it was worth the day before the fire, not what it costs to rebuild today. For a 30-year-old home, this difference can be enormous.

- Replacement Cost Value (RCV): Pays what it costs to rebuild with similar materials at today's prices, without deducting depreciation. This is the standard most homeowners assume they have — but many don't.

- Extended Replacement Cost (ERC): Adds a cushion above your RCV limit, typically 1.25x to 1.5x the dwelling coverage amount (some insurers offer up to 2x). This buffer exists specifically because construction costs spike after disasters.

Code Upgrade Coverage: The Hidden Gap

In WUI fire zones like Pacific Palisades, a post-fire rebuild triggers California Building Code Chapter 7A requirements that simply didn't exist when most policies were written. Mandatory compliance items include:

- Class A fire-rated roofing

- Ember-resistant vents listed to ASTM E2886

- Multi-pane windows with at least one tempered pane

- Ignition-resistant or noncombustible exterior wall assemblies

None of these are optional — and none are cheap. That compliance cost gap is exactly why coverage exists.

California now requires replacement-cost residential policies to include Code Upgrade (Ordinance and Law) coverage of at least 10% of dwelling limits, per the CDI's 2025 Annual Notice. That's additional coverage — it doesn't reduce your dwelling limit. Without it, you pay WUI compliance costs out of pocket.

The Underinsurance Problem

Many California policies were written years ago and haven't kept pace with current labor costs, material prices, or WUI requirements. RAND's research on California wildfire survivors found that 64% reported insufficient coverage to replace or rebuild, and 41% of those who received a settlement said it wasn't enough to complete a rebuild.

Check your declarations page now — before you need it:

- Identify your Coverage A (dwelling) limit and type (ACV vs. RCV)

- Confirm whether ERC is included and at what multiplier

- Locate your Code Upgrade/Ordinance and Law coverage amount

- Review your Loss of Use / Additional Living Expenses (ALE) limit and duration

Loss of Use / ALE Coverage

ALE covers the additional costs of displacement — hotel, meals above your normal baseline, pet boarding, storage. The key word is "additional": if you normally spend $400/month on food, you can claim the amount above that, not the full food bill.

In declared emergencies, California law extends ALE eligibility significantly. To protect that coverage:

- Track every displacement-related receipt from day one

- Request extensions in writing before your current period expires

- Document your normal baseline spending so you can prove the "additional" amount

Don't assume the clock runs out on an arbitrary date — it often doesn't, but you have to ask.

The First 72 Hours: What to Do Immediately

The first 72 hours after a fire determine how much evidence you preserve, how much further damage you prevent, and whether your insurer meets its legal deadlines. Here's what to do:

Secure the property. Board up openings, tarp exposed areas, and check with the fire department about flare-up risk. Failure to mitigate further damage is a claim risk — and these mitigation costs are reimbursable.

Request an advance. Call your insurer before filing a formal claim and ask for an immediate advance for living expenses and necessities. You're entitled to this. Keep every receipt from day one — mitigation costs included.

Document everything. Photograph and video the entire site before anything is cleared or disturbed. Request a copy of the fire department report. This documentation supports — and can make or break — your payout.

Notify your insurer in writing. Under 10 CCR §2695.5, insurers must acknowledge your claim within 15 calendar days, accept or deny within 40 calendar days of receiving proof of claim, and pay within 30 calendar days of acceptance. Written notification creates a paper trail that holds them to these deadlines.

Filing Your Claim and Working With Adjusters

Company Adjuster vs. Public Adjuster

The adjuster who calls you works for your insurance company. Their job is to close your claim efficiently — not to maximize your settlement.

A public adjuster is a licensed professional who works for you. They review your policy, document losses, and negotiate with the insurer on your behalf. Under California law, public adjusters cannot solicit business in a disaster area for 7 calendar days after the event, and in declared disasters, their fees are capped at 10% of the claim settlement.

A public adjuster makes the most sense when:

- Your coverage limits are in dispute

- The insurer's scope of loss underestimates WUI code compliance costs

- Your claim involves complex personal property losses

- You don't have time to manage the process yourself

Build Your Own Scope of Loss

Don't accept the insurer's estimate as the final word. Hire a licensed contractor or independent estimator to prepare a detailed scope that accounts for current WUI code requirements and post-disaster construction pricing. A 2025 Headwaters/IBHS study found that California WUI code requirements alone add approximately $13,070 in material costs for a representative 1,750 sq ft home — before labor, permitting, or post-disaster market premiums.

Your scope and the insurer's scope will differ. That gap is negotiable.

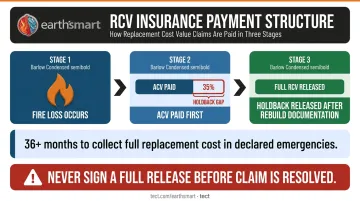

The ACV-First, RCV-Later Payment Structure

If you have RCV coverage, here's how it works in practice:

- The insurer pays ACV first — the depreciated value — while withholding the difference ("holdback")

- You receive the holdback after rebuilding begins and you document costs

- In a declared state of emergency, you have no less than 36 months (plus additional 6-month extensions for good cause) to collect full replacement cost

Never sign a full release before your entire claim is resolved. If you receive a check with full release language, cross it out in writing before cashing it, then send the insurer written notice that the claim remains open. Additional losses are routinely discovered 30 to 90 days after the initial assessment.

Buy vs. Rebuild: Making the Right Decision

California Insurance Code 2051.5

California law gives homeowners a right most don't know they have. Under Insurance Code 2051.5, you can use your full insurance benefits — including ERC and code upgrade coverage — to purchase a replacement home rather than rebuilding on your original lot. The insurer cannot deduct the land value at the new location from your settlement.

SB 495 amendments to this statute take effect January 1, 2026, with full policy compliance required for policies issued or renewed on or after July 1, 2026.

Key Financial Factors

| Factor | Rebuild | Buy Replacement |

|---|---|---|

| Timeline | 18–36+ months (post-disaster markets) | Typically 3–6 months |

| Financing complexity | Construction loan on mortgaged lot | Standard purchase mortgage |

| RCV vs. ACV | Full RCV available if you rebuild | Full RCV available under 2051.5 |

| WUI code costs | Required; partially covered by code upgrade coverage | N/A for existing home |

| Post-disaster pricing | Elevated labor and material costs | Current market pricing |

Rebuild timelines in post-disaster markets are long. The Urban Institute found that roughly 25% of Woolsey Fire homes were rebuilt three years after that event. Paradise has seen stronger progress, but the bottlenecks are real: permitting, contractor availability, materials, and WUI compliance reviews all extend the process.

The Case for Rebuilding Forward

Homeowners who choose to rebuild have an opportunity that doesn't come twice: design the home from the ground up with wildfire resilience, energy performance, and long-term durability built in from day one.

That means assembling your architecture, engineering, and construction team before design begins — so decisions about structure, envelope, and systems align from the start. Early coordination matters because:

- Structural and envelope decisions affect which mechanical systems are viable

- WUI code requirements shape layout, materials, and fire-resistive assembly selection early

- Reworking misaligned decisions mid-design or during construction costs significantly more than getting them right upfront

Rebuilding Smarter: From Recovery to a Resilient Home

What WUI Code Actually Requires

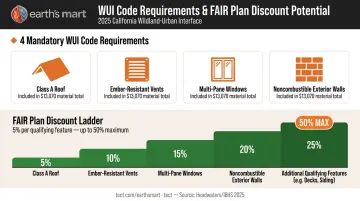

Post-fire rebuilds in California WUI zones trigger CBC Chapter 7A requirements. These aren't optional upgrades — they're the legal baseline for any new construction in a designated Wildland-Urban Interface Fire Area:

- Roofing: Class A fire-rated assembly with no unprotected gaps at roof edges

- Vents: Ember- and flame-resistant vents listed by the California State Fire Marshal or to ASTM E2886

- Windows: Multi-pane glazing with at least one tempered pane (or 20-minute fire-rated alternative)

- Exterior walls: Noncombustible or ignition-resistant materials, or assemblies tested to SFM wildfire exposure standards

- Defensible space: Site-scale requirements in addition to building-level code compliance

Meeting these requirements adds cost: approximately $13,070 in material costs alone for a mid-size California home, per the 2025 Headwaters/IBHS study. That upfront investment, however, directly affects what you pay to insure the home going forward. California's FAIR Plan now offers wildfire-hardening discounts of 5% per qualifying feature (Class A roof, ember-resistant vents, multi-pane windows, noncombustible zone), with a maximum total discount of 50% for fully hardened homes.

The Coordination Problem Nobody Warns You About

Rebuilding a home involves architects, structural engineers, geotechnical engineers, general contractors, and dozens of interconnected product decisions. In most projects, those decisions happen in sequence, not in parallel.

By the time a contractor discovers the structural system conflicts with the specified mechanical equipment, the fix costs far more than it would have caught in week two of design.

Earth'smart powered by tect addresses this through their Earth'smart™ program: one aligned team covering architecture, engineering, construction, permit strategy, and system integration from the start. Through the earth'smart powered by tectApp™ community of 70+ building product manufacturers, homeowners get direct input from the companies behind their materials before anyone locks in those decisions. It's the coordination level commercial projects typically demand, applied to a single-family rebuild.

The goal isn't to restore what was lost. It's a 100+ year home: engineered to withstand fire, flood, and earthquake, designed to reduce insurance costs, and built so it doesn't need to be replaced again.

Frequently Asked Questions

What not to say to a home insurance adjuster?

Avoid speculating about the fire's cause, minimizing damage ("it's mostly cosmetic"), or agreeing verbally to any settlement figure. Never admit anything that could imply fault. Keep all substantive communications in writing and don't finalize anything under time pressure.

What is salvageable after a house fire?

Structural steel and concrete elements may be salvageable pending professional inspection, but wood framing, drywall, insulation, and most personal property exposed to heat and smoke typically are not. Have a licensed structural engineer evaluate any remaining elements before making any decisions.

Should I buy a house that was rebuilt after a fire?

A post-fire rebuild can be a sound purchase if it was done to current Wildland-Urban Interface (WUI) codes with documented permits and inspections. Request the full permit history, as-built drawings, and any engineering or geotechnical reports before proceeding.

How long does it take to rebuild a house after a fire?

In post-disaster California markets, a full rebuild typically takes 18 to 36+ months when accounting for debris removal, permitting, design, and contractor availability. The California Department of Insurance (CDI) has identified permitting delays, material shortages, and contractor scarcity as the most common causes of extended timelines following declared emergencies.

What is the difference between ACV and replacement cost coverage?

ACV pays the depreciated value of what was lost — its market value the day before the fire. Replacement Cost Value (RCV) pays what it costs to rebuild or replace with equivalent materials at today's prices. For an older home in a post-disaster market, the difference can be tens or hundreds of thousands of dollars.