What most homeowners don't know is that documented wildfire hardening can meaningfully reduce those premiums — and in some cases, help them qualify for private coverage again. But the discount structure is specific. Knowing exactly what qualifies makes the difference between leaving money on the table and capturing every discount available.

This guide breaks down how wildfire hardening discounts work, what qualifies under each category, what you can realistically save, and how to approach hardening strategically — whether you're retrofitting an existing home or rebuilding from scratch.

Key Takeaways

- Qualifying for all 12 hardening discounts earns up to 16.4% off the wildfire portion of a California FAIR Plan Dwelling Fire premium

- Discounts fall across four categories: Immediate Surroundings, Structure, Property Level Completion, and Community

- Many Immediate Surroundings discounts cost nothing — clearing debris and maintaining vegetation counts

- Structural upgrades (Class A roof, enclosed eaves, ember-resistant vents) cost more upfront but are far cheaper to specify during a rebuild than to retrofit

- California regulation also requires private insurers to recognize mitigation in their pricing

Why Wildfire Insurance Costs Are Climbing

The carrier retreat from California's high-risk markets has been years in the making. State Farm halted new home insurance sales in California in 2023, citing escalating wildfire losses. They weren't alone. The result: homeowners in fire-prone areas are increasingly landing on the FAIR Plan — the state's insurer of last resort — with fewer options and higher costs.

The numbers tell the story. As of March 2026, the California FAIR Plan reports:

- 684,388 total dwelling and commercial policies in force

- $750 billion in total insured exposure

- $2.02 billion in written premium

Residential enrollment has more than doubled since 2015.

What FAIR Plan Coverage Actually Costs

The FAIR Plan was designed as a backstop, not a primary market — and its pricing reflects that. Homeowners with FAIR Plan coverage in high-risk ZIP codes around Geyserville have paid an average of roughly $11,900 per year, according to San Francisco Chronicle reporting from July 2025.

When your baseline is that high, a 10–16% reduction isn't trivial. On an $11,900 annual premium, even a conservative discount applied to the wildfire portion can translate to hundreds of dollars per year — compounding across the life of the policy.

Home hardening discounts are most valuable in exactly these markets — where premiums are highest and coverage options are fewest.

What Wildfire Home Hardening Discounts Are

Wildfire home hardening discounts are premium reductions that insurers offer to policyholders who take documented steps to make their homes more resistant to wildfire ignition. The California FAIR Plan offers these discounts. Private carriers are also required to offer them — not just encouraged.

10 CCR Section 2644.9, California's "Safer from Wildfires" regulation, took effect October 14, 2022 and expands under new laws starting January 1, 2026. It requires all admitted insurers to account for wildfire mitigation measures in their pricing and to disclose the premium reduction available for each qualifying measure.

One Detail Most Homeowners Miss

Discounts apply to the wildfire portion of the premium, not the total premium amount. The math matters here:

- If wildfire risk is 60% of your total premium, a 16.4% discount applies to that portion only

- On a $5,000 annual premium, that works out to roughly $492 in savings — not the $820 a full-bill discount would suggest

- Actual savings vary based on how your insurer structures the wildfire component

A licensed broker can pull your policy breakdown and calculate the real dollar impact before you invest in hardening measures.

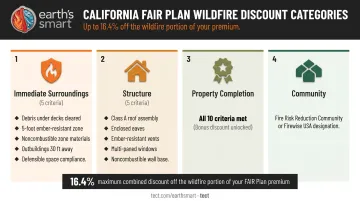

The Four Discount Categories: What Qualifies

The California FAIR Plan's discount structure (updated November 15, 2025) offers up to 12 individual discounts across four categories. Dwelling Fire policyholders can save up to 16.4% on the wildfire portion; Commercial policyholders up to 13.8%.

Immediate Surroundings Discounts (5 criteria)

Most of these cost nothing beyond time — making them the natural first step for any homeowner:

- Clear vegetation and debris from under all decks

- Maintain an ember-resistant clearance zone within 5 feet of the dwelling — no vegetation, debris, or combustible materials

- Use only noncombustible materials (fences, gates, improvements) within that 5-foot zone

- Position combustible sheds and outbuildings more than 30 feet from the structure (or as far as your property allows)

- Comply with California defensible space requirements under Public Resources Code Section 4291 — trees trimmed, brush cleared, full Zone 1 and Zone 2 compliance

Several of these require nothing more than a weekend's work. They qualify immediately and can be verified without contractor involvement.

Structure Discounts (5 criteria)

Structural upgrades require real investment. They're also where fire risk drops most sharply:

- Class A fire-rated roof — asphalt fiberglass, concrete or clay tile, or metal

- Enclosed eaves — open eaves are a primary ember intrusion path

- Ember- and fire-resistant vents with approved wire mesh covering

- Multi-paned windows or functional shutters

- Noncombustible material along the bottom 6 inches of all exterior walls

For homes being retrofitted, these upgrades range from targeted (vent screens, wall base treatment) to significant (full roof replacement, soffit enclosure). For homes being rebuilt from scratch, specifying these materials at the design phase adds minimal marginal cost — they're standard selections, not expensive add-ons.

Property Level Completion Discount

Satisfying all 10 criteria across both Immediate Surroundings and Structure categories earns an additional bonus discount. Partial completion doesn't qualify. Getting to nine criteria and stopping leaves the completion bonus — often the largest single discount in the structure — on the table.

Community Discount

Properties in a qualifying community program earn an additional discount on top of individual criteria savings. Two independent programs qualify:

- Fire Risk Reduction Community — certified by the California Board of Forestry

- Firewise USA Site in Good Standing — verified through NFPA's site finder

Check both lists separately. Qualifying for either adds to your discount; qualifying for both compounds it.

The Real Math: Costs, Savings, and the Investment Case

What Hardening Actually Costs

According to UC ANR research, retrofitting a typical 2,000-square-foot California home can range from $2,000 to over $100,000 depending on scope. Many effective strategies — debris clearing, vent upgrades, noncombustible wall base treatment — fall in the $2,000–$15,000 range. Full structural retrofits including roof and eave enclosure sit at the high end.

The good news: you don't have to do everything at once. Each qualifying criterion earns an incremental discount. A homeowner who clears vegetation, removes combustibles from the 5-foot zone, and meets defensible space requirements has already qualified for multiple Immediate Surroundings discounts — before touching the structure.

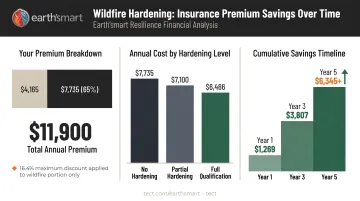

A Realistic Savings Example

Take a homeowner in a Very High Fire Hazard Severity Zone paying $11,900/year on a FAIR Plan Dwelling Fire policy, with wildfire risk representing 65% of that premium (~$7,735 wildfire portion).

- At full qualification (all 12 discounts, up to 16.4% off the wildfire portion): ~$1,269/year savings

- On an Immediate Surroundings-only path (partial qualification): discounts still apply, typically in the 5–10% range depending on which criteria are met

Over five years, full qualification represents over $6,000 in cumulative savings — before factoring in any improvement in private market access or policy reinstatement.

The Risk Reduction Argument

Those dollar figures only tell part of the story. UC Berkeley research published in August 2025 found that home hardening combined with defensible space can double the number of structures that survive a blaze, with Zone Zero vegetation removal alone reducing structure losses by 17%, and community-wide mitigation cutting wildfire damage by as much as 50%.

A hardened home isn't just cheaper to insure. It's far more likely to still be standing.

Maximizing Discounts: Retrofitting vs. Rebuilding

The Retrofit Path

For homeowners in existing homes:

- Audit your current compliance — go through all 12 criteria and identify what you already meet

- Start with Immediate Surroundings — clear debris, establish the 5-foot zone, achieve defensible space compliance. These are low-cost and qualify immediately

- Phase structural upgrades — prioritize vent replacement and wall base treatment before larger projects like roof replacement

- Work with a licensed broker — you cannot apply to the FAIR Plan directly. Your broker submits documentation and coordinates discount eligibility

- Ensure genuine compliance — all properties claiming discounts are subject to inspection. Discounts can be removed if criteria aren't met at inspection time

Why Rebuilding Is the Better Opportunity

When rebuilding after a wildfire, every structural decision starts from a blank slate. Specifying a Class A roof, ember-resistant vents, enclosed eaves, noncombustible wall base, and multi-paned windows at the design phase adds negligible marginal cost compared to retrofitting those same features into an existing structure.

The structural discount category can be locked in from day one. Retrofits layer these improvements over years; a rebuild captures them all at once.

That front-loaded approach is how earth'smart powered by tect works with homeowners rebuilding in Pacific Palisades, the North Bay, East Bay Hills, Lake Tahoe, and other high-risk California markets. Through the Earth'smart™ delivery model, wildfire hardening specifications — Class A roofing, non-combustible eaves and soffits, ember-resistant venting, fire-resistive wall assemblies — are specified at the concept-design phase, not corrected after construction begins.

The earth'smart powered by tectApp™ community of 70+ vetted building product manufacturers means the companies behind these systems are involved early. Compliance is built into the specification from the start, not verified at the end.

Earth'smart powered by tect also produces insurance-aligned documentation packages that brokers and underwriters can use directly to support coverage and pricing decisions. Each package covers:

- System-level performance specifications

- Manufacturer documentation for all hardening assemblies

- Defensible-space coordination records

- IBHS Wildfire Prepared Home alignment evidence

For homeowners trying to exit the FAIR Plan, that documentation gives brokers and underwriters the evidence they need to support private-market coverage.

Frequently Asked Questions

How much can homeowners save on insurance from wildfire hardening discounts?

The California FAIR Plan offers up to 16.4% off the wildfire portion of a Dwelling Fire premium for policyholders who qualify for all 12 hardening discounts. Private admitted carriers operating under the Safer from Wildfires framework apply their own discount structures, so total savings vary by insurer.

What is the 5-foot rule in California for wildfire hardening?

California's 5-foot rule requires homeowners to maintain an ember-resistant clearance zone within five feet of the dwelling — clearing all vegetation, debris, mulch, and combustible materials. Any improvements within that zone (fences, gates) must also use only noncombustible materials to qualify for the corresponding FAIR Plan discount.

Do all California insurers have to offer wildfire hardening discounts?

Yes. California's Safer from Wildfires framework (10 CCR Section 2644.9) requires all admitted insurers — not just the FAIR Plan — to account for wildfire risk reduction in their pricing and to disclose the premium reduction available for each qualifying mitigation measure. Specific discount amounts and structures vary by carrier.

Do I need a professional inspection to qualify for wildfire hardening discounts?

All FAIR Plan properties claiming discounts are subject to inspection to verify eligibility, and discounts may be removed if the property doesn't meet stated criteria at inspection time. Document every improvement with photos, receipts, and material specs before you apply.

Can wildfire home hardening help me get back on the private insurance market?

Documented hardening can improve a property's wildfire risk rating, making it more attractive to private carriers operating under the Safer from Wildfires framework. Several major carriers have committed to writing policies for homes earning IBHS Wildfire Prepared Home designations. Working with an advisor who understands both the hardening requirements and how carriers evaluate them gives you the clearest picture of your re-entry options.