That gap matters. Construction type is one of the most direct variables insurers use to assess fire risk, set your premium, and decide whether to offer coverage at all. In high-risk areas like Pacific Palisades, the wrong classification — or the wrong construction — can mean higher deductibles, limited carrier options, or no coverage from standard insurers.

This guide breaks down the six ISO construction classifications used across the insurance industry, explains what each means for your policy, and shows how material choices during design and construction directly affect what you'll pay for insurance over the life of your home.

Key Takeaways

- Construction type classifies a home's fire risk based on the materials used in its walls, floors, roof, and structural frame.

- ISO defines six classes — Class 1 (Frame, highest risk) through Class 6 (Fire Resistive, lowest risk).

- Most U.S. homes are Class 1 or Class 2 — the highest-risk, highest-premium categories.

- Masonry, non-combustible, or fire-resistive materials qualify a home for lower premiums and broader coverage.

- In wildfire-prone areas, construction type determines insurability, not just price.

What Are Construction Types for Insurance?

Construction type is an insurance classification based on the primary materials used in a home's structural components — exterior walls, floors, roof, and structural frame — along with how well those materials resist fire.

The Insurance Services Office (ISO) developed a standardized system of six construction classes (Codes 1–6) that insurers use to rate properties. Verisk confirms that properly identifying construction class helps underwriters rate risk more accurately. These classes form the backbone of how fire risk is priced in most homeowners policies.

ISO Classes vs. Building Code Types

Homeowners sometimes confuse ISO construction classes with the International Building Code's (IBC) Types I–V, which architects and code officials use. They're related but serve different purposes:

- IBC Types I–V — building code categories governing what materials can be used during construction

- ISO Classes 1–6 — insurance rating categories that determine your premium and coverage terms

- Key distinction — IBC types shape how a home is built; ISO classes shape what you pay to insure it

Both systems evaluate fire resistance and materials, but only ISO classes directly affect your insurance costs. A home can be built to IBC Type III standards and still fall into ISO Class 1 depending on how its structural frame is constructed.

Construction type has nothing to do with a home's size, age, or appearance. A brick-faced home is not automatically a higher ISO class — if the structural frame beneath that brick veneer is wood, insurers classify it as Frame (Class 1).

Why Your Home's Construction Type Matters for Insurance

Construction type shapes three things insurers care about most: premium cost, deductible structure, and coverage eligibility.

The NAIC's Consumer's Guide to Home Insurance confirms that homes built primarily with brick or masonry typically carry lower premiums than wood-frame homes. The premium difference comes down to fire behavior: combustible materials ignite faster and produce larger, harder-to-contain losses.

The Misclassification Problem

Many homeowners unknowingly misreport their construction type — and the consequences show up at claim time. NAIC guidance notes that if dwelling coverage falls below 80% of full replacement cost, insurers may reduce what they pay on a claim. When construction type is misclassified, replacement cost estimates are often inaccurate, leaving homeowners underinsured without realizing it.

The Wildfire Zone Multiplier

In Wildland-Urban Interface (WUI) communities, construction type directly determines access to coverage, not just price. California's insurance market shows how fast this shift is happening:

- FAIR Plan's share of California residential policies grew from 1.6% in 2015 to 3.7% in 2023, with 324,954 policies in force

- Residential surplus-lines policies jumped from 24,659 in 2022 to 41,514 in 2023

- In California's 10 highest-wildfire-exposure counties, FAIR Plan market share rose from 1% in 2015 to 22% in 2021

Frame homes in fire-prone areas are increasingly being declined by standard carriers, pushing homeowners into surplus-lines or residual markets where coverage is thinner and premiums are higher. Understanding which construction type your home falls into — and what that classification means — is the starting point for addressing that risk.

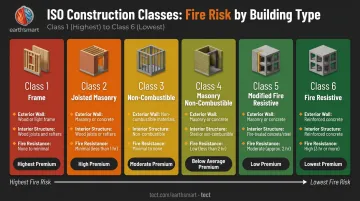

The 6 ISO Construction Types for Homes

The ISO system moves from Class 1 (most combustible) to Class 6 (most fire-resistant). Understanding where your home falls is the starting point for understanding your insurance costs.

Here's how all six classes compare at a glance:

| ISO Class | Common Name | Exterior Walls | Interior Structure | Fire Resistance | Insurance Tier |

|---|---|---|---|---|---|

| Class 1 | Frame | Wood or veneer over wood | Wood framing | None | Highest risk |

| Class 2 | Joisted Masonry | Brick, block, stone, adobe | Wood floors/roof | Partial | Moderate-high |

| Class 3 | Non-Combustible | Metal or gypsum | Metal framing | Partial | Moderate |

| Class 4 | Masonry Non-Combustible | Masonry (4"+ or 1-hr rated) | Non-combustible | Moderate | Lower |

| Class 5 | Modified Fire Resistive | All components | All components | 1–2 hours | Low |

| Class 6 | Fire Resistive | All components | All components | 2+ hours | Lowest |

Frame (Class 1)

Frame construction includes any home built primarily with wood framing — walls, floors, and roof. This includes homes with brick veneer, stone veneer, or stucco exteriors where the structural frame beneath is still wood.

This is the most common construction type in the U.S., with NAHB reporting that wood framing accounted for 94% of completed single-family homes in 2024.

Insurance implication: Highest risk classification, highest base premiums. In fire-prone regions, Class 1 homes are most likely to face coverage restrictions or difficulty obtaining coverage from standard carriers.

Joisted Masonry (Class 2)

Joisted Masonry homes have true masonry exterior walls — brick, concrete block, stone, or adobe — but combustible wood-framed floors and roof. The exterior resists fire better than Class 1, but the interior structure is still combustible.

Insurance implication: Slightly more favorable rates than Frame, but interior fire risk remains elevated. Insurers treat this as moderate-to-high risk for residential properties.

Non-Combustible (Class 3)

Non-Combustible construction uses metal, gypsum, or other non-combustible materials for all exterior walls and structural supports — no wood framing in the primary structure. More common in commercial construction, but applicable to steel-framed residential builds.

Insurance implication: A lower risk rating than Classes 1 or 2. However, without fire-resistance treatment, steel loses structural integrity under prolonged heat — placing this class in the moderate range rather than the lowest tier.

Masonry Non-Combustible (Class 4)

Masonry Non-Combustible combines masonry exterior walls with non-combustible (metal or equivalent) floors and roof — meaning both the exterior and interior structural elements are free of combustible material.

Per Verisk, exterior walls must be masonry at least 4 inches thick or carry a minimum 1-hour fire-resistance rating.

Insurance implication: A substantial improvement over Classes 1–3. The combination of masonry walls and non-combustible interior structure significantly limits fire spread, typically resulting in lower premiums and better coverage terms.

Modified Fire Resistive (Class 5)

Modified Fire Resistive construction requires the full building envelope — walls, floors, and roof — to withstand fire for at least 1 hour but less than 2 hours. Typical of mid-rise structures, but achievable in high-performance residential construction with the right assemblies.

Coverage impact: Significant risk reduction compared to standard residential construction. Insurers typically offer more competitive premiums and broader coverage, and in high-risk areas, Class 5 expands the pool of carriers willing to write the policy.

Fire Resistive (Class 6)

Fire Resistive is the highest classification. All structural components must withstand fire for 2 or more hours, typically using reinforced concrete, protected steel, or equivalent systems.

That's not a minor upgrade — it's a different category of building.

Coverage impact: Lowest fire risk rating in the ISO system. Class 6 homes qualify for the most favorable premiums and coverage structures. In wildfire-prone areas, building to this standard can be the difference between insurable and uninsurable.

How Construction Type Affects Your Insurance Premium

The relationship is direct: higher ISO class number equals lower fire risk equals lower base premium. NAIC confirms that brick and masonry homes consistently carry lower premiums than wood-frame homes — and in high-risk markets, the gap is widening.

Beyond the base premium, construction type shapes several other coverage variables:

- Deductible structure — Frame homes in wildfire zones often carry higher wildfire-specific deductibles

- Coverage exclusions — Class 1 homes may face exclusions for fire-related losses in certain markets

- Carrier access — Standard carriers increasingly decline Class 1 homes in WUI zones, pushing homeowners into surplus-lines markets

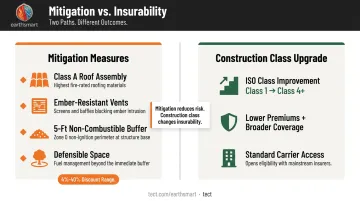

What Mitigation Can and Can't Do

Fire-risk mitigation measures can qualify for meaningful discounts. California's Safer from Wildfires program requires insurers to offer discounts ranging from 4% to 40% for qualifying actions, which include:

- Class A fire-rated roofs

- Ember-resistant vents

- 5-foot non-combustible buffer zones

- Defensible space clearance

That said, mitigation doesn't change the underlying ISO construction class. A Frame home with excellent defensible space is still a Frame home. These measures reduce modeled risk and can improve insurer decisions at the margins — but they don't reclassify the structure. If better insurability is the goal, the materials you build with matter more than the measures you add after.

How to Build or Rebuild Toward a Better Construction Class

Construction class is not fixed by location or neighborhood — it's determined by the decisions made during design and construction. For homeowners rebuilding after wildfire or building new in high-risk areas, every rebuild is a direct opportunity to choose a higher class.

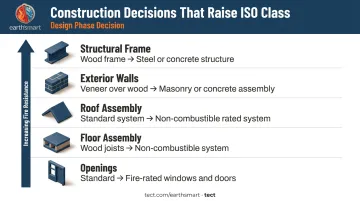

The Decisions That Move the Needle

Achieving a higher ISO class comes down to a specific set of material and system decisions:

- Structural frame — Switch from wood framing to steel or concrete structural systems

- Exterior walls — Use masonry or concrete instead of wood-frame with stucco or veneer

- Roof assembly — Specify non-combustible roof systems with rated fire-resistance hours

- Floor assembly — Use non-combustible floor systems rather than wood joists

- Openings — Specify fire-rated windows and doors to limit ignition pathways

These decisions must be made early in the design phase to be effectively integrated. Specifying a fire-resistive wall assembly mid-construction — after the frame is up — creates coordination problems, cost overruns, and often compromised performance. FEMA's Builder's Guide for Wildfire Zones identifies wind-driven embers as the primary cause of home ignition and recommends exterior wall materials like cement board, masonry, and three-coat stucco — materials that need to be designed in, not retrofitted.

The Cost of Building Better

A 2025 report from IBHS and Headwaters Economics found that building a 1,750-square-foot home to California WUI Code Part 7 standards adds roughly $13,070 over standard construction costs. California's Department of Insurance estimates that rebuilding a $500,000 home to wildfire-resistant standards costs approximately 2% to 3% more — around $13,000 to $15,000.

That upfront investment needs to be weighed against lower premiums, better coverage terms, and — in some markets — the ability to obtain coverage at all.

Why Coordination Matters More Than Materials Alone

Spending more on materials only pays off if those materials work as a system. Achieving Class 4, 5, or 6 requires walls, floors, roof, and structural frame to be rated and integrated together — not selected independently by separate trades. In conventional fragmented construction, product decisions happen too late, teams aren't aligned, and critical system interactions get resolved in the field rather than in the design.

Earth'smart powered by tect's work with homeowners rebuilding in Pacific Palisades and surrounding WUI communities is structured around solving this problem early. Through the earth'smart powered by tectApp™ community of 70+ building product manufacturers, fire-resistive assemblies, non-combustible structural systems, and integrated suppression strategies are specified together from the start — with direct input from the manufacturers behind those systems. For homeowners rebuilding after the 2025 Palisades fires, that early alignment is what determines what ISO class the finished home actually achieves.

Frequently Asked Questions

What are construction types for insurance?

Construction types are standardized ISO classifications (Classes 1–6) based on the materials used in a home's walls, floors, roof, and structural frame. Insurers use these classifications to assess fire risk and set premiums, with Class 1 (Frame) carrying the highest risk and Class 6 (Fire Resistive) the lowest.

How does construction type affect home insurance premiums?

Higher-risk classes like Frame (Class 1) typically result in higher base premiums, higher wildfire deductibles, and more limited coverage options. Fire-resistive classes (5–6) generally qualify for lower premiums and broader coverage, with a larger pool of standard carriers willing to write the policy.

What construction type are most homes?

The majority of U.S. residential homes are Frame (Class 1) due to widespread wood-frame construction (NAHB reports wood framing accounted for 94% of completed single-family homes in 2024). This places most homes in the highest-risk, highest-premium insurance category.

What is the best construction type for homes in wildfire-prone areas?

Masonry Non-Combustible (Class 4) through Fire Resistive (Class 6) offer the best insurance outcomes in wildfire-prone areas. These classifications reflect materials that resist ignition and slow fire spread, making homes more insurable in markets where standard carriers are increasingly declining Frame homes.

Can rebuilding my home improve its construction classification?

Yes. A rebuild is a direct opportunity to choose higher-class materials and systems. Decisions made during the design phase — about structural framing, wall assemblies, and roof materials — directly determine what ISO class the finished home achieves.

What is the difference between ISO construction classes and IBC construction types?

IBC Types I–V are building code classifications used by architects and code officials during design and permitting. ISO Classes 1–6 are the insurance industry's rating system. Both evaluate fire resistance and materials, but ISO classes directly affect your premiums and coverage terms.