Introduction

Insuring a new construction home isn't a single transaction — it's two separate cost events that most homeowners don't plan for simultaneously.

The first is builder's risk insurance, which covers the structure during construction. The second is standard homeowners insurance, which begins at closing. Each phase runs on different cost logic, different coverage triggers, and different gaps — and most homeowners only discover this at the worst possible moment.

The good news: new construction homes are cheaper to insure than older homes. According to The Zebra, new builds average $966/year versus $1,670/year for a 20-year-old home with equivalent coverage. That advantage depends heavily on location, materials, and how cleanly you manage the handoff between phases.

This guide covers both cost phases, what drives premiums up or down, and the planning gaps that tend to surface most often for homeowners in high-risk areas rebuilding from the ground up.

Key Takeaways

- New construction insurance has two phases: builder's risk (during construction) and homeowners insurance (at closing) — budget for both from the start

- Builder's risk typically costs 1–4% of total construction value per year

- New homes cost roughly 73% less to insure than 20-year-old homes on average — but that gap narrows fast

- Location is the biggest premium driver: high-risk states can cost 172% above the national average

- Premiums can jump 53% when a home hits the 10-year mark

How Much Does New Construction Insurance Cost?

Costs vary significantly by phase, location, home value, and carrier. There's no universal rate for new construction. That's part of the problem. Homeowners who only budget for the post-closing phase often find themselves unprotected or underfunded during the build.

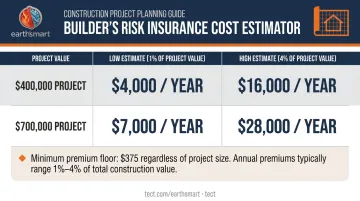

Builder's Risk Insurance (During Construction)

Builder's risk is priced as a percentage of the total completed construction value — meaning hard costs like materials, labor, and foundation. Land value is excluded from the calculation.

According to Insureon, the standard planning benchmark is 1%–4% of completed construction value per year. Here's what that looks like in practice:

| Completed Construction Value | 1% (Low Estimate) | 4% (High Estimate) |

|---|---|---|

| $400,000 | $4,000/year | $16,000/year |

| $700,000 | $7,000/year | $28,000/year |

A few practical notes on builder's risk costs:

- Minimum premiums apply. Zurich's residential builder's risk program sets a $375 minimum premium in most states — relevant for smaller projects where the percentage calculation falls below that floor

- Project type matters. New construction typically prices lower than renovation because it starts from a clean slate with fewer unknowns. Installation floaters (for equipment or fixtures) are generally the least expensive of the three

- Policy terms are typically structured on an annual basis, with renewal options for up to two additional years depending on project timeline

Homeowners Insurance Cost After Closing

Once the home is complete, standard homeowners insurance takes over. National benchmarks from Insurify and Bankrate show general coverage-tier averages:

| Dwelling Coverage | Insurify National Average | Bankrate National Average |

|---|---|---|

| $300,000 | $2,604/year | $2,424/year |

| $500,000 | $3,972/year | — |

| $750,000 | $5,688/year | $5,254/year |

Important caveat: these are national averages across all home ages. New construction homes typically cost meaningfully less, with new-build averages closer to $966/year before location risk premiums are applied.

Regional variation can overwhelm the new-construction discount entirely. Bankrate reports Nebraska averages $6,587/year for $300K dwelling coverage, which is 172% above the national average, while Vermont averages just $827/year.

Builder's Risk vs. Homeowners Insurance: Two Phases, Two Costs

The core distinction: builder's risk protects the structure during construction; homeowners insurance protects the completed home after closing. Most homeowners need both, and the transition between them must be seamless.

Phase 1: Builder's Risk Insurance

Who buys it: In most cases, the general contractor carries builder's risk. But homeowners building custom homes or acting as owner-builders need their own policy. Lenders always require proof of coverage before releasing construction loan funds.

If a builder carries the policy, homeowners should:

- Confirm the policy's coverage limits and term dates

- Ask to be named as an additional insured

- Verify what happens if the construction timeline extends beyond the policy term

What builder's risk covers:

- The structure under construction

- Materials stored on-site and in transit

- Temporary structures (scaffolding, site offices)

Common exclusions (often requiring separate endorsements):

- Flood and earthquake

- Workers' compensation

- Professional liability

- Employee theft

Phase 2: Homeowners Insurance

Standard homeowners insurance — typically an HO-3 or HO-5 policy — begins at closing. It covers nothing from the construction phase. A standard policy includes:

- Dwelling and other structures

- Personal property

- Loss of use

- Liability and medical payments

One decision carries real financial weight: replacement cost vs. actual cash value. Insuring to actual cash value is a costly mistake — depreciation deductions leave a gap between what the insurer pays and what rebuilding actually costs. Always insure to full replacement cost.

Given that NAHB has reported lumber prices surged more than 300% during the 2020–2021 period before partial recovery, and building material costs remain elevated, the home may cost substantially more to rebuild today than it did to build. Extended replacement cost coverage — which extends the dwelling limit by 10%–50% depending on the insurer — provides a buffer against this gap.

Key Factors That Affect Your New Construction Insurance Cost

Both builder's risk and homeowners insurance premiums respond to the same underlying variables, but location and construction quality carry the most weight.

Location and Hazard Zone

Location is the single largest underwriting variable. Homes in the following areas carry significant premium surcharges:

- FEMA flood zones — standard policies exclude flood; the average NFIP flood policy costs $926/year nationally

- Wildfire-prone areas — including WUI zones like Pacific Palisades, where insurer availability has contracted sharply

- Tornado corridor states — Oklahoma City averages $5,554/year, 129% above the national average

Standard homeowners policies also exclude earthquake, requiring a separate policy in high-seismic zones.

In high-risk wildfire markets, price is only part of the challenge — availability is the bigger constraint. California's FAIR Plan exists specifically for homeowners who cannot obtain coverage through a standard carrier.

The California Department of Insurance has enacted a mandatory one-year moratorium on cancellations and non-renewals in areas adjacent to fire perimeters following a declared emergency. Even so, the underlying availability constraints remain a real consideration for anyone rebuilding in WUI zones.

Construction Materials and Build Quality

Materials affect both builder's risk pricing and long-term homeowners insurance premiums — combustible construction means higher claim probability, and insurers price accordingly.

- Wood-frame construction carries the highest fire risk among common construction types

- Concrete masonry, steel framing, and fire-rated assemblies earn more favorable underwriting

- IBHS FORTIFIED designation may qualify homes for homeowners insurance discounts in participating states

Earth'smart powered by tect's Earth'smart™ approach for Pacific Palisades rebuilds addresses this directly. Exterior walls use fire-resistive pre-insulated concrete masonry, non-combustible materials and assemblies run throughout, and integrated on-site fire suppression systems are standard. By resolving risk at the system level rather than meeting code minimums, these homes are built for an insurance landscape where coverage is harder to obtain and premiums keep climbing.

Home Value, Coverage Limits, and Deductibles

- Dwelling coverage must equal full replacement cost, not market value. For new construction, actual build cost is a useful starting point, but current reconstruction costs may be higher

- Deductible selection directly affects premium. The Insurance Information Institute notes that raising a deductible from $500 to $1,000 can save up to about 25%, depending on the home, insurer, and location

- Higher deductibles reduce annual cost but increase out-of-pocket exposure at claim time — a trade-off worth modeling before finalizing a policy

How to Lower Your New Construction Insurance Costs

Some cost factors are fixed by location and home value. Others are negotiable decisions made at build time or policy inception.

Discounts most relevant to new construction:

- New home discount — one of the largest available discounts; applies to homes typically under 2 years old

- Home-auto bundling — averages 30% savings on homeowners premiums, or roughly $268/year, according to Policygenius and The Zebra

- Burglar alarm — typically saves about 3%

- Smoke alarm — approximately 0.4% savings

- Wind mitigation or fire-resistant materials — discounts exist but aren't uniformly published nationally; ask each carrier directly — they're not always advertised

Beyond standard discounts, a few decisions at the start of your policy can have an outsized impact on long-term costs.

Three strategies that often get overlooked:

- Shop multiple carriers at inception. Premium spreads between the cheapest and most expensive carriers on identical homes can be substantial. An independent agent with access to both admitted and surplus lines markets can find better terms, particularly in high-risk zones

- Consider multi-year rate guarantees. Some carriers offer rate locks for new construction — worth exploring before the home ages into higher pricing brackets

- Document your fire-resistive and resilient features. Homes built with fire-resistive assemblies, FORTIFIED designations, or integrated suppression systems may qualify for insurer credits — but only if you can prove it. Having material specifications and system documentation ready when you apply makes those credits accessible rather than theoretical.

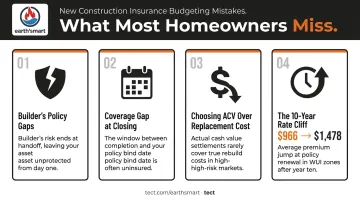

What Most Homeowners Miss When Budgeting for New Construction Insurance

Builder's policy gaps. If the contractor's builder's risk policy has gaps, lapses, or doesn't name the homeowner as an additional insured, the homeowner carries uninsured risk. Verify coverage details before construction starts.

The coverage gap at closing. The period between builder's risk ending and homeowners insurance beginning is a real exposure window. An insurance binder can bridge short gaps if the construction timeline shifts — coordinate policy dates precisely.

Choosing ACV over replacement cost. Insuring a new home to actual cash value rather than replacement cost is a common mistake. Depreciation deductions at claim time can leave the homeowner well short of full rebuild cost, especially given recent construction cost increases.

The 10-year rate cliff. New construction pricing doesn't hold indefinitely. According to The Zebra, premiums rise from $966/year for new construction to $1,478/year at 10 years — a 53% increase.

Proactive steps to soften that transition include maintaining a claims-free record, documenting system updates, and exploring multi-year rate agreements before the home ages into higher-cost brackets. For homes built with non-combustible materials in wildfire-prone areas, the underlying risk profile may support a stronger underwriting conversation at the 10-year mark — but that conversation has to start before the renewal, not after.

Conclusion

Insuring a new construction home is a two-phase process, and misjudging either phase creates budget surprises or real coverage gaps.

The "right" cost depends on where the home is, how it's built, how coverage is structured, and which carrier underwrites it. In lower-risk inland markets, new construction's age-based pricing advantage is meaningful and durable.

In high-risk WUI zones like Pacific Palisades, that advantage requires active management. Location risk, insurer availability, and replacement-cost inflation can all work against the homeowner simultaneously.

Homes built with resilient, fire-resistive materials don't just perform better through a fire event. They address the underlying risk factors that drive insurance decisions — which is exactly what earth'smart powered by tect's Earth'smart™ approach does. Building to minimum code is no longer enough in today's risk environment.

Design-stage decisions determine which carriers will write the policy, which risk category the home falls into, and whether that advantage holds over time. That's the difference between a home that ages into a coverage problem and one that doesn't.

Frequently Asked Questions

How much does new home construction insurance cost?

Two costs to budget for: builder's risk typically runs 1%–4% of total construction value per year (with a $375 minimum premium in most states), and homeowners insurance after closing averages around $966/year for new construction nationally. Location and home value are the biggest variables in both phases.

Is it cheaper to insure a new construction home?

Yes. New builds average $966/year versus $1,670/year for a 20-year-old home, roughly 73% less. Modern building codes, updated materials, and new systems reduce claim probability. That advantage narrows around the 10-year mark, when premiums can jump approximately 53%.

How much does a $1,000,000 liability insurance policy cost?

Standard homeowners policies include $100K–$500K in liability coverage. For $1M or more in protection, most homeowners add a personal umbrella policy , which costs an average of $383/year for $1 million in coverage, according to a Bankrate-cited ACE Private Risk Services study.

When do I need homeowners insurance on new construction?

Homeowners insurance must be active at closing. Lenders require proof before final loan approval, and closing typically runs 30–45 days from a signed purchase agreement. Builder's risk covers construction, so coordinate the two policies to avoid any coverage gap.

What discounts are available for new construction homeowners insurance?

Common discounts include the new home discount, home-auto bundling (averaging 30% savings), smart home and security system credits, fire-resistant material credits, and claims-free history. Most are most valuable in the first few years, so enroll early while the home still qualifies as new construction.