The confusion is understandable. The VHFHSZ designation carries real consequences, but it doesn't work the way most homeowners assume. There's no separate insurance product for fire hazard zones. What changes is your access to coverage, your costs, and your options — and understanding that distinction early can save you significant money and stress.

Key Takeaways

- No separate "VHFHSZ insurance" product exists — standard homeowners insurance remains the goal, but becomes significantly harder to secure in high-risk zones

- CAL FIRE's hazard maps don't set your insurance rates — insurers use their own parcel-level wildfire models, which may score your property differently than the official zone designation

- VHFHSZ homeowners often face higher premiums, non-renewals, or limited coverage from private carriers

- Verified home hardening (defensible space, non-combustible materials, fire-resistant assemblies) is one of the most direct ways to improve your insurability

- For homeowners rebuilding after wildfire, the construction phase is the highest-leverage moment to directly change your risk profile

What Is a Very High Fire Hazard Severity Zone?

CAL FIRE and the Office of the State Fire Marshal classify California land into three Fire Hazard Severity Zone tiers: Moderate, High, and Very High. The classification uses a science-based model that evaluates long-term physical hazard factors — not just whether a fire has burned there recently.

Factors that determine FHSZ classification include:

- Vegetation type, density, and fuel load

- Topography and slope

- Historical fire weather patterns

- Ember production and travel distance (burning embers can ignite structures up to 1 mile from the main fire)

- Proximity to wildland areas

SRA vs. LRA: Why the Distinction Matters

There are two separate classification systems that often get conflated:

- State Responsibility Areas (SRA): Mapped directly by CAL FIRE. Updated SRA maps became effective April 1, 2024.

- Local Responsibility Areas (LRA): Designated by local jurisdictions following State Fire Marshal recommendations. LRA rollout occurred in phases through 2025.

Pacific Palisades falls under the City of Los Angeles's LRA Very High designation — meaning local ordinances, not state maps alone, govern the fire safety requirements that apply there. You can check your specific parcel on CAL FIRE's Fire Hazard Severity Zone Viewer.

What FHSZ Designations Actually Do

Knowing your zone is only half the picture. What matters is what that designation actually requires of you — and here the answer surprises most homeowners: FHSZ designations drive building codes and defensible space laws, not insurance rates.

A Very High classification means you're subject to:

- Chapter 7A wildfire-resistant construction requirements

- Mandatory defensible space under Public Resources Code Section 4291

- Local WUI fire safety regulations

It does not mean your insurer is required to charge you a specific premium or apply a specific underwriting rule.

Do You Need Special Insurance for a Very High Fire Hazard Severity Zone?

The short answer: no. There is no distinct insurance product called "Very High Fire Hazard Severity Zone insurance." Standard homeowners insurance — typically an HO-3 policy — remains the right vehicle. It covers fire as a named peril and includes dwelling, personal property, other structures, and additional living expenses.

So why does the question keep coming up?

The VHFHSZ Label Still Changes Everything Practically

Being in a Very High zone flags your property to insurers and triggers stricter scrutiny. It doesn't require a different type of coverage — it makes coverage harder to get. The designation correlates with the risk factors insurers care about, even if it doesn't directly dictate their decisions.

The California Department of Insurance has clarified that CAL FIRE hazard maps are not used by insurance companies for rate-setting or underwriting decisions. Insurers use their own proprietary wildfire catastrophe models that score properties at the parcel level — factoring in topography, fuel loads, fire suppression capacity, and structure-specific data. Your home may score higher or lower than the FHSZ map alone would suggest.

What This Means Practically

If you're in a VHFHSZ, you absolutely still need homeowners insurance — more urgently than in lower-risk areas. The core questions become:

- Whether you can still obtain coverage from a standard private carrier

- What mitigation steps improve your chances of staying insured

- How your property scores on insurer risk models, not just FHSZ maps

For homeowners rebuilding after wildfire, that last point matters most. A newly constructed home built to current fire-resistance standards often scores better on insurer models than the home it replaced. Rebuilding isn't just restoration — it's a concrete opportunity to improve your risk profile from the ground up.

How a VHFHSZ Designation Affects Your Coverage and Costs

Higher Premiums

The California statewide average homeowner insurance premium is $1,571 annually, according to NAIC data cited by the California Department of Insurance — above the $1,512 national average. For homeowners in high-fire-risk areas, costs climb further, though the precise surcharge varies by insurer, location, and property characteristics. The VHFHSZ classification itself doesn't set the rate, but it correlates strongly with the risk factors that do.

Non-Renewals and Market Exit

This is where many California homeowners have felt the sharpest impact. CDI data shows residential non-renewals increased 31% from 2020 to 2021 alone. Major carriers have reduced or exited California's high-risk market — not because of individual homeowner risk, but as portfolio-level business decisions.

California law does provide a safeguard: under Senate Bill 824 (2018), there is a mandatory one-year moratorium on cancellations or non-renewals in ZIP codes within or adjacent to a Governor-declared wildfire disaster area. Once that year expires, homeowners in affected areas need to actively reassess their coverage options.

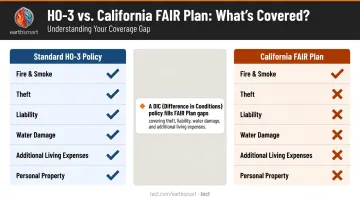

The FAIR Plan: Coverage of Last Resort

When private carriers decline coverage, the California FAIR Plan becomes the backstop. The FAIR Plan now represents approximately 4% of California's residential market (based on 2023 figures), with 668,609 homeowner and commercial policies reported.

Key facts about FAIR Plan coverage:

- Covers losses from fire, lightning, internal explosion, and smoke

- Does not cover theft, liability, water damage, or additional living expenses

- Homeowners typically need a Differences in Conditions (DIC) policy to fill those gaps

- The FAIR Plan + DIC combination is generally more complex and more costly than a standard HO-3 policy

Coverage Restrictions to Watch For

Even when private coverage is available, policies in high-risk areas may include:

- Wildfire-specific deductibles separate from the standard deductible (often structured as a percentage of dwelling coverage rather than a flat dollar amount)

- Sublimits that cap what the insurer pays for wildfire-related losses

- Actual cash value treatment instead of replacement cost for certain structures

- Exclusions for specific conditions or outbuildings

Before signing, ask your insurer specifically whether wildfire losses are subject to a separate deductible, whether sublimits apply to your dwelling, and how damaged outbuildings are valued. The answers will vary — and they matter.

Your Insurance Options When Standard Coverage Becomes Difficult

Private Carriers With Mitigation Incentives

Not every private insurer has left California's high-risk market. Some continue writing policies with requirements or discounts tied to verified wildfire mitigation steps.

If your home has documented fire-resistance features, you're in a stronger negotiating position when shopping for coverage. Documented features that carry weight include:

- Defensible space compliance

- Class A fire-rated roof materials

- Ember-resistant vents

- Non-combustible siding

Excess and Surplus (E&S) Lines

Surplus lines insurers cover risks that standard admitted carriers won't. They operate with more flexible rate and form structures, which means they can write policies where others won't. The trade-offs:

- Generally higher premiums than admitted market alternatives

- Not subject to the same rate and form regulation as admitted insurers

- No state guaranty fund protection — an important consumer protection that disappears in the E&S market

Working with an independent agent who has access to E&S markets is essential if you've been declined by standard carriers.

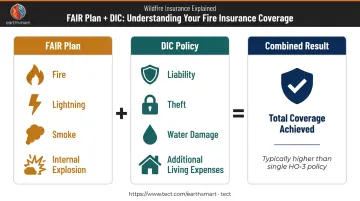

California FAIR Plan + DIC Policy

When E&S markets are inaccessible or unaffordable, this combination satisfies mortgage lenders' minimum requirements and provides meaningful coverage — but the limitations matter:

- FAIR Plan: Fire, lightning, internal explosion, smoke

- DIC policy: Fills gaps — liability, theft, water damage, additional living expenses

- Combined cost: Typically higher than a single standard HO-3 policy

- Coverage quality: Less comprehensive than what a competitive private market policy would provide

For most homeowners, improving the fire-resistance of the home itself — not just insurance shopping — is what ultimately reopens access to better coverage options.

How Reducing Your Home's Fire Risk Can Change Your Insurance Picture

Defensible Space: The Legal Baseline

CAL FIRE's defensible space law applies in SRA zones and VHFHSZ in LRA zones. The three zones:

- Zone Zero (0–5 feet): Remove all combustible material immediately around the home — the "ember-resistant zone"

- Zone 1 (5–30 feet): Vegetation management to reduce fuel continuity

- Zone 2 (30–100 feet): Fuel reduction to slow fire spread

Insurers may verify defensible space compliance before writing or renewing a policy. This isn't just a safety measure — it's a documented risk factor they look at directly.

Structural Features That Reduce Wildfire Ignition Risk

The IBHS Wildfire Prepared Home Technical Standard identifies the specific structural features that most directly reduce ignition risk:

- Vents: Noncombustible mesh with openings no larger than 1/8 inch

- Roofing: Class A fire-rated covering or tested Class A assembly

- Eaves: Enclosed with noncombustible material (fiber-cement, stucco, or metal)

- Siding: Minimum 6 inches of noncombustible material at the base of exterior walls

- Decks: Noncombustible components for new construction

These features matter for insurance because insurers are increasingly using structural data — not just location — to adjust premiums and make underwriting decisions.

California's Safer from Wildfires Regulation

Under 10 CCR Section 2644.9, effective October 14, 2022, insurance companies are required to offer discounts to homeowners who take verified wildfire mitigation steps. The regulation requires a separate credit for each qualifying mitigation factor.

Per NFPA's Firewise USA program, California regulations also require insurers to recognize Firewise USA community designations and provide discounts to property owners in those communities.

Mitigation only affects your insurance picture if you can document it — through photos, contractor records, third-party assessments, or program participation. Undocumented improvements don't earn you credits.

Building Forward, Not Just Rebuilding

Documentation matters — but only if the underlying improvements are there to document. For homeowners in Pacific Palisades and other VHFHSZ communities rebuilding after wildfire, the construction phase is the highest-leverage moment available. A home rebuilt to minimum code looks complete but may score no better than what existed before, because code minimums aren't what today's insurer risk models reward.

Earth'smart powered by tect integrates non-combustible systems from the structural level through the building envelope: fire-resistive exterior wall systems using pre-insulated concrete masonry, dedicated on-site water supply for fire events, and site-scale fire suppression using a vapor dome system. Rather than treating fire resistance as a surface upgrade, these decisions are made early in design — with direct input from the earth'smart powered by tectApp™ community of 70+ building product manufacturers behind the materials.

The outcome is a home engineered to withstand fire exposure and documented to reduce risk — built specifically for the insurance landscape homeowners face today, not the one that existed a decade ago.

Frequently Asked Questions

What are the fire hazard severity zones in California?

CAL FIRE designates three tiers — Moderate, High, and Very High — across State Responsibility Areas, using factors like fuel load, terrain, fire weather, and ember production. Local jurisdictions designate zones in Local Responsibility Areas. Updated SRA maps took effect April 1, 2024, with LRA rollout continuing through 2025. Check your parcel at the CAL FIRE FHSZ Viewer.

What is considered high risk for home insurance?

Insurers assess wildfire risk using proprietary catastrophe models that factor in location, vegetation density, topography, fire history, proximity to fire services, and the physical characteristics of the home itself. A property can score high on these models regardless of its official FHSZ classification, and the reverse is equally true.

Does being in a Very High Fire Hazard Severity Zone mean I can't get home insurance?

No. A VHFHSZ designation doesn't automatically disqualify a home from coverage, but it does make finding affordable private insurance more difficult. Homeowners who are declined by standard carriers can explore excess and surplus lines insurers (specialized carriers for hard-to-place risks) or the California FAIR Plan as a last resort.

Will my standard homeowners insurance cover wildfire damage if I'm in a VHFHSZ?

Fire is a covered peril under standard HO-3 policies. However, policies in high-risk areas may include separate wildfire deductibles, sublimits, or exclusions. Review your policy terms carefully: don't assume full replacement coverage applies without reading the specific conditions.

How can I lower my home insurance premium in a Very High Fire Hazard Severity Zone?

Verified mitigation — documented defensible space, ember-resistant vents, fire-resistant roofing and siding — can qualify homeowners for discounts under California's Safer from Wildfires regulation (10 CCR Section 2644.9). Documentation and third-party verification are essential. Undocumented improvements don't earn credits with insurers.

What is the California FAIR Plan and when do I need it?

The FAIR Plan is a state-backed insurer of last resort for homeowners who can't obtain coverage from private carriers. It covers fire, lightning, internal explosion, and smoke, but not liability, theft, or water damage. Most homeowners pair it with a Differences in Conditions policy to fill those gaps — it's more expensive and less comprehensive than standard private coverage, though it does satisfy basic lender requirements.