The consequences are concrete: State Farm announced in March 2024 that it would non-renew approximately 30,000 California homeowners policies. Farmers restricted new homeowners policies in California starting July 2023. In this environment, a Class A fire-rated roof isn't a nice-to-have — it directly affects whether you can get coverage, what you pay for it, and how a claim gets settled.

This article explains the specific insurance outcomes tied to Class A roofing: premium discounts, coverage eligibility, claims treatment, and what happens without one.

Key Takeaways

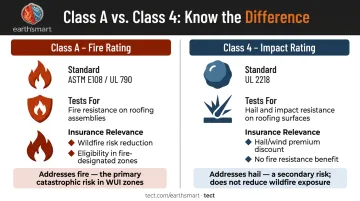

- Class A is a fire-resistance rating under ASTM E108/UL 790 — not to be confused with Class 4 impact resistance (UL 2218); insurers treat these separately

- California's wildfire mitigation discount programs range from 4%–40% depending on actions taken, with a Class A roof as a qualifying factor

- In high-risk fire zones, a Class A roof can determine whether a policy gets issued or renewed at all

- Without one, expect actual cash value settlements, steeper deductibles, and potential fire damage exclusions

- Document and report the roof to your insurer — without that step, the insurance benefit never kicks in

What Is a Class A Fire Rating?

Class A is the highest fire-resistance classification for roofing, defined under ASTM E108 and UL 790. The tests measure three things: surface flame spread, resistance to burning brand ignition (simulated ember exposure), and performance under intermittent flame exposure.

The 2022 California Building Code (CBC) Chapter 15 defines Class A assemblies as those effective against severe fire test exposure — the baseline standard in wildfire-prone regions.

The Assembly Rule Most Homeowners Miss

The rating applies to the full roofing assembly — not just the shingle or tile you can see. The deck, underlayment, and covering must be tested together as a system. A Class A-listed shingle installed over a non-compliant underlayment or deck may not produce a Class A-rated assembly. If the assembly isn't verified as a listed system, an insurer may not recognize it as Class A — even if the shingle label says otherwise.

Class A vs. Class 4: A Critical Distinction

These are entirely separate classification systems, and confusing them is common:

| Rating | Standard | Tests For | Insurance Relevance |

|---|---|---|---|

| Class A | ASTM E108 / UL 790 | Fire resistance | Wildfire risk reduction, eligibility in fire zones |

| Class 4 | UL 2218 | Impact resistance (hail) | Hail/wind discount, separate from fire |

In California and other fire-exposed states, insurers look at Class A status — not Class 4. Texas DOI's roofing credit program, by contrast, targets impact-resistant roofing under UL 2218 and has no bearing on fire ratings.

Common Class A-Rated Materials

- Asphalt fiberglass composition shingles (when assembly-listed)

- Standing seam metal and metal shingles

- Concrete and clay tile

- Slate (on noncombustible decks)

- Fire-retardant-treated wood shakes (only when the full assembly is tested and listed)

Untreated wood shakes do not qualify under any assembly configuration.

How Class A Roofs Lower Your Insurance Premiums

Insurance pricing is built on probability and cost of claims. A Class A roof reduces both the likelihood of fire-related damage and the severity of a resulting loss. Insurers price that reduced risk directly into your premium.

What the Discount Data Actually Shows

The verified numbers are program-specific, not universal. Here's what's documented:

- California DOI (March 2026 briefing): Wildfire mitigation discounts across all qualifying actions range 4%–40%, with a Class A roof as one of the qualifying factors

- California FAIR Plan (November 2025): Dwelling policyholders who meet all 12 hardening criteria — including a Class A roof — may receive up to 16.4% off the wildfire portion of their premium

- USAA Colorado: Lists a Class A fire-rated roof as worth 1% off the wildfire-related premium as a standalone factor

No single universal percentage applies across all carriers. The range reflects carrier-specific filings, state programs, and how many other mitigation measures the homeowner has in place.

Geographic Amplification

The discount scales with risk. In California, Colorado, and Texas — where wildfire and wind exposure are built into base rates — the savings from a Class A roof are larger than in low-risk markets. A fire-hardened roof in Pacific Palisades means more to your insurer than the same roof in a low-hazard ZIP code.

That geographic weighting connects directly to how underwriters score your property. The higher the regional risk, the more each of these factors shifts your rate.

What Underwriters Actually Measure

When setting premiums, underwriters evaluate specific rating factors that a Class A roof directly influences:

- Fire risk score — reduced by fire-resistant materials

- Roof condition rating — improved by new or recently inspected materials

- Estimated remaining useful life — longer for metal, tile, and slate vs. standard asphalt

- Rebuild/replacement cost per square foot — affected by material durability and lifespan

Metal and tile roofs last longer, which lowers how often insurers expect to price in a replacement — and that factors into your base rate.

A new Class A-rated roof and a fire-resistance discount can compound. Confirm stacking eligibility with your specific carrier, since this isn't guaranteed across all policy forms.

How Class A Roofs Protect Your Insurability in High-Risk Fire Zones

Premium discounts matter. But in the highest-risk markets, getting coverage at all is the more pressing issue.

The California Market Reality

CBS News reported in June 2023 that both Allstate and State Farm halted new policy sales in California. Farmers restricted new homeowners policies starting July 3, 2023. State Farm's 30,000 non-renewal announcement in 2024 followed. The California DOI's Safer from Wildfires framework now requires insurers to provide discounts for verified mitigation actions — and a Class A fire-rated roof is explicitly listed as a qualifying action.

As a result, many carriers treat Class A roofing as a minimum eligibility condition in designated high-hazard zones. A non-rated or degraded roof may trigger non-renewal regardless of willingness to pay a higher premium.

Replacement Cost vs. Actual Cash Value

Policy valuation terms create a significant financial gap that roof condition directly affects:

- Replacement cost (RCV): Pays to rebuild with similar kind and quality — no depreciation deducted

- Actual cash value (ACV): Deducts depreciation from the payout, often leaving homeowners short on rebuild funds

Homes with older, non-Class-A roofs are more likely to be settled on ACV terms. Class A-rated roofs in good condition improve the likelihood of qualifying for full RCV coverage — though the final valuation method depends on policy terms, not roof rating alone.

The FAIR Plan Is a Backstop, Not a Solution

California's FAIR Plan exists for homeowners who can't get standard market coverage. It provides basic fire insurance with residential coverage limits up to $3 million, but premiums are higher and coverage is more limited than standard policies.

A Class A roof, paired with other fire-hardening features, improves a homeowner's chances of qualifying for standard market coverage rather than being pushed into the residual market.

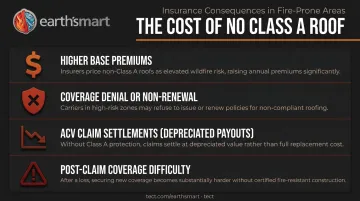

What Happens Without a Class A Roof in High-Risk Areas

For homeowners in fire-exposed areas, the gap between a rated and unrated roof shows up directly in coverage terms and claim outcomes:

- Higher base premiums — non-rated roofs represent higher fire risk, priced accordingly

- Coverage denial or non-renewal — some carriers restrict issuance in fire zones based on roof condition or rating

- ACV claim settlements — older, non-compliant roofs are more likely to receive depreciated payouts

- Post-claim replacement difficulty — after a fire-related claim, finding a new carrier becomes harder

Code Requirements Add Another Layer of Exposure

Those insurance consequences don't exist in isolation — California's building code reinforces them. The 2022 CBC Chapter 15 requires Class A roof coverings in designated Fire Hazard Severity Zones for new structures, and for existing structures when more than 50% of the total roof area is replaced within a one-year period. Section 705A CBC extends this further: Class A or higher applies to all roofs in remodel and alteration projects in WUI-designated areas.

A homeowner doing a partial re-roof after wildfire damage may trigger a full Class A compliance requirement. Non-compliance at rebuild time creates permitting obstacles that delay recovery, and can affect coverage terms on the rebuilt home.

How to Get the Most Insurance Value from a Class A Roof

Installing a Class A roof is step one. The insurance benefit is only realized when you complete the steps that follow.

Documentation Is Non-Negotiable

California DOI's Safer from Wildfires rules state that insurers may require proof that a mitigation action was completed, or may require an inspection. The documentation you'll typically need includes:

- Manufacturer certification for the tested assembly

- Contractor installation forms confirming the assembly configuration

- Building permit records

- Mitigation verification forms (required by some carriers and FAIR Plan)

The FAIR Plan's wildfire hardening discount form specifically defines the Class A fire-rated roof criterion and the evidence required to claim it. Submit documentation proactively.

Confirm Material and Assembly Eligibility First

Not every Class A product qualifies for every carrier's fire-resistant roof discount. Confirm with your insurer:

- Which specific materials and assembly configurations they recognize

- Whether the discount applies to the full premium or only the wildfire-related portion

- What evidence format they require (inspection, form, or manufacturer documentation)

Get the Assembly Right from the Start

For homeowners rebuilding after wildfire or undertaking a full re-roof, material decisions made at this stage have long-term financial consequences. The roofing material, underlayment, and adjacent envelope systems need to be specified together — not independently — to ensure the assembled system achieves and maintains its Class A classification.

Early coordination between materials, contractors, and documentation is what prevents costly reclassification later. Earth'smart powered by tect's WUI rebuild process connects homeowners with the earth'smart powered by tectApp™ community of 70+ building product manufacturers, so assembly decisions, permit strategy, and documentation are aligned from the start — not corrected after the fact.

Frequently Asked Questions

How much will my homeowners insurance go down if I get a new roof?

The range depends on material, fire or impact rating, age improvement, and location. California's DOI reports wildfire mitigation discounts of 4%–40% across qualifying actions, with FAIR Plan policyholders meeting all 12 hardening criteria eligible for up to 16.4% off the wildfire portion. Class A-rated materials in fire-prone areas typically land at the higher end.

What is the 25% rule for roofing?

The verified California trigger under CBC Chapter 15 is replacing more than 50% of total roof area within one year in a Fire Hazard Severity Zone — which mandates Class A compliance for the entire roof, not just the repaired section. Some insurers apply their own thresholds, but 50% is the confirmed state standard.

What materials qualify for a Class A fire rating?

Common Class A-rated materials include concrete and clay tile, standing seam metal, slate, asphalt fiberglass composition shingles, and fire-retardant-treated wood shakes. What matters is that the full roofing assembly — underlayment and deck included — must be tested together to achieve the rating, not just the surface material.

Is a Class A roof required in wildfire-prone areas of California?

Yes. California's 2022 CBC Chapter 15 and Chapter 7A require Class A roof coverings on new construction and on re-roofing projects that exceed the 50% threshold in designated Fire Hazard Severity Zones. Local WUI ordinances, such as Marin County's, extend this to essentially all roofing work in WUI areas.

Can a Class A roof help me get homeowners insurance in a high-risk fire zone?

A Class A roof is one of the most significant eligibility factors in high-risk markets, and it materially improves access to standard-market policies rather than expensive last-resort options like the FAIR Plan. No single feature guarantees coverage, but paired with defensible space, ember-resistant vents, and non-combustible siding, the combination carries real weight with underwriters.