Most homeowners have never filed a total-loss claim. They don't know what "ALE" means, whether to talk to a contractor before the adjuster visits, or whether rebuilding even makes financial sense. That uncertainty — compounded by displacement, stress, and an inbox full of vendors — is where costly mistakes begin.

This guide covers the full arc: what to do in the first 72 hours, how to navigate your insurance claim, the rebuild-versus-relocate decision, and what a complete reconstruction actually looks like step by step. It's written primarily for homeowners in wildfire-prone areas like Pacific Palisades and other Wildland-Urban Interface (WUI) communities, but the framework applies to any total-loss fire situation.

Key Takeaways

- Safety first — don't re-enter your property without official clearance; fire debris contains toxic materials

- Contact your insurer within 24–48 hours and document all damage before any cleanup begins

- ALE coverage typically pays for temporary housing — confirm your limits with your insurer and save every receipt

- Rebuilding vs. relocating is a real decision; review your full policy before committing to either path

- The rebuild process takes 12–24+ months — knowing each phase helps you sidestep delays and contractor mistakes

What to Do in the First 72 Hours After Your House Burns Down

The first three days after a fire set the trajectory for everything that follows. Acting in the wrong order — or skipping steps under stress — can cost you money, documentation, and options you won't get back.

Don't Re-Enter Without Clearance

LA County Public Health warns that ash and debris from burned structures can contain asbestos, arsenic, lead, and other carcinogens. Cal/OSHA classifies fire cleanup as hazardous work requiring formal hazard identification and controls. Personal protective equipment is mandatory, not optional.

Wait for official clearance from fire authorities. When you do re-enter, wear an N95 mask, gloves, goggles, and long sleeves. Use wet cleaning methods or a HEPA vacuum — never dry-sweep.

Activate Your ALE Coverage Immediately

Your homeowner's policy almost certainly includes Additional Living Expenses (ALE) or "Loss of Use" coverage. Per the California Department of Insurance, ALE covers:

- Temporary rent or hotel costs

- Extra food costs beyond your usual budget

- Extra transportation and mileage

- Storage and furniture rental during displacement

Call your insurer and ask specifically about ALE before you book anything. Save every receipt from the moment you left your home. In California wildfire catastrophe situations, ALE coverage lasts at least 24 months with potential extensions — but dollar limits can still run out.

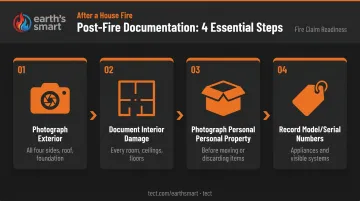

Document Everything Before Touching Anything

Before any cleanup, debris removal, or salvage attempts:

- Photograph and video the entire exterior — all four sides, the roof, the foundation

- Document interior damage in every room, including ceilings and floors

- Photograph personal property in place, before it's moved or discarded

- Record model numbers and serial numbers of appliances and systems where visible

This documentation is your insurance claim. Once debris is moved or removed, that record cannot be reconstructed.

File Your Claim and Request the Incident Report

Contact your insurer within 24–48 hours, even before you know the full extent of damage. Simultaneously, request the official fire incident report from your fire department — in Los Angeles, this goes through LAFD's Fire Records/CPRA process. Having both documents in hand before your adjuster arrives puts you in a much stronger position.

Access Disaster Relief Resources

Don't overlook immediate assistance programs:

- American Red Cross — emergency shelter, food, and basic needs

- FEMA Individual Assistance — available if a federal disaster declaration has been issued for your area

- Local nonprofits and community funds — often faster than government programs for immediate needs

Check disasterassistance.gov to confirm whether a federal declaration has been issued. That determination unlocks FEMA grants and SBA disaster loans.

Rebuild, Repair, or Walk Away? How to Decide

Three real paths exist after a total or partial loss, and each carries different financial and timeline implications.

| Path | Best When | Key Consideration |

|---|---|---|

| Partial repair/restoration | Damage is localized; structure is sound | Cost advantage depends on what's salvageable |

| Full rebuild on same lot | Total loss; strong location ties; favorable policy | Requires engineering, permits, full code compliance |

| Sell the lot and relocate | Coverage is insufficient; local regulations limit rebuild | Outstanding mortgage still owed regardless |

Neither decision should move forward without a licensed structural engineer assessing what remains — and without a full read of your insurance policy.

The Financial Reality of Rebuilding

After a major wildfire, demand for licensed contractors, specialty materials, and permit capacity spikes — and rebuild costs rise with it. The California DOI explicitly notes that demand surge is a primary reason insurer estimates understate true rebuild costs. Get at least one independent licensed contractor estimate before accepting any insurer figure.

That pricing reality compounds the two misconceptions that most often cost homeowners money.

Two Misconceptions That Cost Homeowners Money

Misconception 1: A mortgage forces you to rebuild. It doesn't. You still owe the outstanding loan balance, but you're not required to rebuild on the lot. Fannie Mae and Freddie Mac both offer disaster forbearance — up to 12 months of reduced or suspended payments — for eligible borrowers. Contact your lender before making any rebuild commitments.

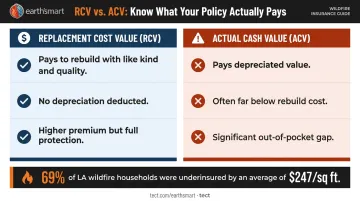

Misconception 2: Your policy covers the full rebuild cost. It might — or it might fall well short. The difference comes down to how your policy values the loss:

- Replacement Cost Value (RCV): Pays to rebuild with like kind and quality, no depreciation deduction

- Actual Cash Value (ACV): Pays depreciated value — often far below actual rebuild cost

A 2025 United Policyholders survey of Los Angeles wildfire households found 69% were underinsured by an average of $247 per square foot. Before accepting any settlement, verify whether your policy type, coverage limits, and any extended replacement cost endorsements actually close that gap.

Navigating Your Insurance Claim After a House Fire

Your insurance claim is the primary financial mechanism of your recovery. Most homeowners have never read their full policy. That unfamiliarity gets costly when urgency is high.

How the Claims Process Works

The sequence, per NAIC's post-disaster guide:

- File your claim immediately

- Adjuster inspects and documents damage

- Scope of loss is determined

- Insurer issues a settlement offer

- You review, negotiate, or supplement if needed

Insurers issue a first offer — not a final one. You have the right to dispute it and submit your own licensed contractor estimates. Don't sign anything final until you've compared the insurer's scope against at least one independent bid.

What to Document for a Strong Claim

- Contents inventory: Itemized list of belongings, estimated values, purchase dates, photos

- Structural damage: Photos and video of all affected areas

- Emergency receipts: Temporary housing, food, clothing — from day one

- Contractor estimates: At least one independent licensed contractor assessment

Coverage Types to Understand

- Dwelling coverage — rebuilding costs for the physical structure, including foundation and attached systems

- Personal property coverage — contents and belongings, typically at actual cash value unless you carry replacement cost coverage

- ALE/Loss of Use — hotel, rental, and meal costs during displacement, usually capped at 20–30% of dwelling coverage

- Ordinance or Law (Code Upgrade) coverage — this one surprises people

Code upgrade coverage pays the additional cost of rebuilding to current building codes, which may be far more stringent than when your home was originally built. Without it, that gap comes out of your pocket. Ask your insurer specifically whether this endorsement is on your policy.

Even with solid coverage, many homeowners face a shortfall. When that happens, other funding options can fill the gap.

When Insurance Isn't Enough

If your coverage falls short, other options exist:

- FEMA Individual Assistance grants — up to $42,500 per household (if a federal disaster declaration applies)

- SBA Physical Disaster Loans — up to $500,000 for homeowners, at rates not exceeding 4% for those unable to obtain credit elsewhere

- Construction or home equity loans — for creditworthy homeowners with equity in the land

- Nonprofit and community relief programs — often faster to access than federal programs

The House Rebuild Process: Step by Step

From cleared lot to certificate of occupancy, a full rebuild typically takes 12–24 months — and in large wildfire events, considerably longer. Urban Institute research shows that after the Camp Fire, only 23% of destroyed homes had certificates of occupancy after 6.5 years. Community-scale recovery is slower than individual rebuilds. Start organized, and you stay ahead of the queue.

Step 1: Site Assessment, Clearance, and Debris Removal

Before a single foundation form goes in, the site must be cleared in a specific sequence:

- Structural assessment — a licensed engineer evaluates whether any foundations, walls, or framing can be retained

- Hazardous materials inspection — asbestos, lead, and toxic fire residue must be professionally identified

- Phase 1 debris removal — EPA and DTSC manage removal of pressurized cylinders, batteries, pesticides, and bulk asbestos

- Phase 2 debris removal — ash, remaining debris, and contaminated soil; in LA County wildfire events, CalRecycle or the Army Corps of Engineers may handle this if homeowners submit a Right-of-Entry form

Debris removal must be completed before permit applications will be accepted. Don't skip or rush it — Phase 2 involves soil scraping and independent testing before clearance is issued.

Step 2: Design, Permits, and Contractor Selection

Once the site is cleared, design and permitting run in parallel. An architect prepares plans compliant with current building codes — which may be substantially different from the codes in effect when your home was originally built.

Those code differences make early coordination critical. Firms like earth'smart powered by tect bring one coordinated team across architecture, engineering, and construction — and connect clients to the earth'smart powered by tectApp community of 70+ building product manufacturers so material and systems decisions are made correctly from the start.

Getting manufacturer input during design, rather than mid-construction, prevents the costly change orders and schedule overruns that derail most rebuilds.

On contractor selection: verify license and insurance on the CSLB database, check references, and require a written fixed-price contract. Under California law, down payments cannot exceed $1,000 or 10% of the contract price, whichever is less.

Step 3: Construction, Inspections, and Move-In

Construction proceeds in a defined sequence:

- Foundation and framing

- Mechanical, electrical, and plumbing rough-in

- Insulation and envelope

- Finishes and systems commissioning

- Final inspections and certificate of occupancy

Each phase requires scheduled inspections under the California Building Code. Skipping or rushing inspections creates liability and can block your certificate of occupancy — which blocks your ability to move back in and your insurer's final payment.

Stay in regular contact with both your contractor and your insurance adjuster throughout construction. Changes in scope must be documented and approved to protect your claim.

Don't Just Rebuild — Build Forward

A fire rebuild forces you to bring your home up to current code. That's the starting point, not the finish line. Homeowners who rebuild strategically treat this as a rare opportunity to construct a home that performs better in the next fire — not just one that meets the same standard as the one that burned.

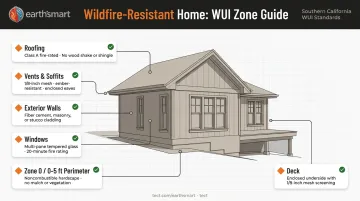

What Fire-Resistant Construction Actually Requires in WUI Areas

The IBHS Wildfire Prepared Home standard (2025) and California's Chapter 7A building codes set clear performance targets:

- Roofing: Class A fire-rated material tested to ASTM E108 or UL 790; wood roofing is prohibited regardless of rating

- Vents and soffits: Corrosion-resistant with 1/8-inch mesh or ASTM E2886 flame/ember compliance — enclosed eaves block ember intrusion

- Exterior walls: 6-inch vertical noncombustible base clearance; fiber cement, masonry, or stucco cladding for Plus-level certification

- Windows: Multi-pane with at least two tempered panes, or minimum 20-minute fire rating

- Zone 0 (0–5 feet): Noncombustible hardscape immediately around the structure — this is where most ember ignition events start

- Decks: Enclosed with 1/8-inch mesh when surface is 4 feet or less above grade

The California DOI's Safer from Wildfires program offers insurance discounts for each of these measures — exact percentages vary by insurer, but the cumulative effect can meaningfully improve both your premium and your insurability in high-risk zones.

The Integration Advantage

Choosing materials individually is not the same as engineering a home that performs as a system. Earth'smart powered by tect brings architecture, engineering, and construction under one coordinated team, with direct input from the manufacturers behind the materials. That alignment means decisions are made correctly from the start, not corrected mid-construction.

For a WUI rebuild, that coordination translates to fire-resistive exterior wall assemblies using pre-insulated concrete masonry, non-combustible materials throughout, long-life structural systems, and on-site water supply integrated with site-scale fire suppression. The goal is a home built to exceed today's code and last 100+ years.

Common Mistakes Homeowners Make During Fire Rebuild

Rushing Contractor Selection

Post-disaster contractor demand creates conditions where unlicensed operators market aggressively to displaced homeowners. The CSLB warned specifically after the 2025 Southern California fires that scams and poor workmanship are concentrated risks during this period.

Avoid by:

- Verifying license status at cslb.ca.gov before any conversation advances

- Requiring a written scope and fixed-price contract

- Never paying more than $1,000 or 10% upfront

- Getting at least two to three bids — the lowest rarely reflects true quality

Accepting the First Insurance Settlement

Many homeowners discover mid-rebuild that their coverage limit was set years ago at figures that don't reflect current construction costs. Accepting the initial adjuster estimate without independent contractor verification leaves real money on the table.

Two rules protect your claim:

- Don't start demolition or extensive cleanup before the adjuster completes their assessment

- Once evidence is disturbed, your ability to supplement the claim drops sharply

Rebuilding to the Same Standard

Settling a claim and choosing a contractor are decisions you can revisit. The materials and systems that go into your rebuild are not. If your original home wasn't built to WUI fire-resistant standards, rebuilding to minimum code puts you in exactly the same position when the next fire comes through.

This is a one-time decision. The framing, envelope, mechanical systems, and materials that go in during this rebuild will define your home's performance and your family's safety for decades.

Frequently Asked Questions

Can you rebuild your house after a fire?

Yes, most fire-damaged or destroyed homes can be rebuilt, but the path depends on structural assessment results, local zoning, code compliance, and insurance coverage. In some WUI zones, new planning regulations may restrict what can be rebuilt — check with your local planning department early.

How long does it take to rebuild a house after a fire?

Small repairs can take weeks; a full rebuild after total loss typically takes 12–24 months or longer. LA permit issuance averaged about 85 days in late 2025, but community-scale wildfire recovery — clearance, permitting, contractor availability, material lead times — routinely extends every phase beyond individual estimates.

Is it cheaper to gut a house or rebuild it?

Gutting and restoring a partially damaged home is often less expensive because foundations, framing, and utilities may be reusable. That cost advantage shrinks or disappears with severe structural damage. A full rebuild also allows for design upgrades and improved code compliance that add measurable long-term value.

Do you still have to pay your mortgage if your house burns down?

Yes — the mortgage obligation continues even after total loss. Contact your lender immediately; Fannie Mae and Freddie Mac both offer disaster forbearance options that may allow reduced or suspended payments for a period. Insurance proceeds are typically applied first toward the outstanding loan balance.

How long does it take for smoke smell to leave after a fire?

Light smoke odor can clear in days with ventilation. Deep penetration into walls, insulation, and HVAC systems requires professional remediation — ozone treatment is sometimes used, though the EPA notes it has limitations and generates its own indoor byproducts.

What fire-resistant materials should I use when rebuilding in a wildfire-prone area?

Key materials to prioritize:

- Roofing: Class A fire-rated (metal, tile, or approved composite)

- Cladding: Non-combustible fiber cement, stucco, or masonry

- Windows: Multi-pane tempered glass

- Eaves and soffits: Fully enclosed to block ember intrusion

Selections should align with California's Chapter 7A requirements and be reviewed by an architect experienced in WUI fire-resilient design.