This is the defining tension of the wildfire insurance crisis: mitigation spending is accelerating, and so are cancellations.

This article explains why that disconnect exists, what the data shows about who actually falls through the coverage gap, which mitigation steps insurers and catastrophe models actually score, and why the rebuild moment — not the retrofit moment — is when homeowners can most fundamentally change their long-term risk profile.

Key Takeaways

- Communities are doing the work, but insurers are making zone-level exit decisions — not property-level ones

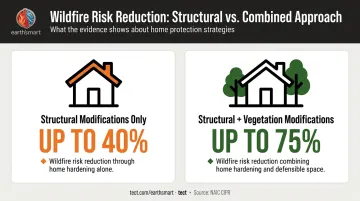

- Structural modifications can reduce wildfire risk up to 40%, per a 2020 NAIC report — but that finding hasn't reached most underwriting decisions

- The California FAIR Plan now carries 684,388 policies and $750 billion in total exposure, with many homeowners unable to find coverage elsewhere

- California's December 2024 catastrophe-modeling rules open a path for mitigation to influence rates — contingent on insurer filings and model approvals

- Rebuilding after wildfire is the clearest opportunity to produce a risk profile that future insurers can score differently

The Mitigation Paradox: Spending Tens of Thousands, Still Getting Dropped

The Frustration Is Real — and Structural

Residents install Class A roofing, replace combustible wood siding, clear defensible space to code, and remove outbuildings — then receive non-renewal notices anyway. This isn't an anomaly. It's a pattern that has frustrated homeowners, fire chiefs, and elected officials across California's wildfire-affected counties.

The core reason is structural: insurance companies are not making renewal decisions based on individual home risk. They are managing portfolio-level exposure. When a carrier decides to exit a ZIP code or reduce its footprint in a high-risk region, even a well-hardened home on a cleared lot gets caught in that sweep. The decision is a zone decision, not a property decision.

Where the Regulatory Gap Lives

California's insurance commissioner has authority over rate-making: meaning mitigation can, in theory, influence what you pay. But the commissioner does not have authority over underwriting decisions. An insurer can decline to write or renew policies in a given area regardless of individual property improvements. Those are two different legal mechanisms.

That distinction matters. Mitigation can reduce your premium if your insurer stays — but it doesn't legally prevent them from leaving.

The gap widens at the verification level. There is no standardized, widely adopted process for homeowners to document mitigation efforts in a way that insurers are required to recognize. A December 2025 Resources for the Future working paper found that wildfire mitigation discounts vary significantly across insurers and are often small relative to actual retrofit costs.

The Science Exists — The Underwriting Doesn't Always Follow

The NAIC's CIPR report found that structural modifications can reduce wildfire risk up to 40%, and combined structural and vegetation modifications can reduce risk up to 75%. These are modeled maximums, not guaranteed premium reductions. The science supports mitigation. What hasn't kept pace is any consistent obligation for insurers to factor that risk reduction into renewal decisions.

What the Data Reveals: The Growing Insurance Gap

The FAIR Plan Is a Warning Signal, Not a Solution

The California FAIR Plan — the state's insurer of last resort — has grown to 684,388 total dwelling and commercial policies, carrying $750 billion in total exposure as of March 2026. That growth reflects how many homeowners have been pushed out of the private market.

But the less-reported story is what happens to homeowners who lose private coverage and don't land on the FAIR Plan. Authoritative data on the exact migration rate is not publicly available, but research indicates a meaningful gap — homeowners who neither secure private coverage nor enroll in the FAIR Plan, ending up with no coverage at all.

Self-Insuring Is a Riskier Choice Than It Sounds

Homeowners who have paid off their mortgages are not legally required to carry insurance. Some, facing FAIR Plan premiums that feel disproportionate to their perceived risk, choose to go uninsured. The personal financial exposure is real. Less discussed is the community-level consequence: uninsured properties damaged by wildfire may sit vacant or abandoned for years, stalling neighborhood recovery and suppressing surrounding property values.

The Coverage Cap Problem in High-Value Markets

The FAIR Plan's residential coverage limit was doubled to $3 million in 2019 in response to rising home values and construction costs. In markets like Pacific Palisades — where pre-fire home values and current rebuild costs regularly exceed that threshold — even homeowners who do migrate to the FAIR Plan may be substantially underinsured relative to what it would actually cost to rebuild.

Beyond the coverage cap, the FAIR Plan carries other structural limitations:

- Does not include liability protection (typically carried through private policies)

- Offers no bundled endorsements for additional living expenses during rebuild

- Leaves meaningful gaps for homeowners whose rebuild costs exceed $3 million

For communities where the risk reduction work is already done, these gaps mean the insurance system isn't rewarding the right behavior — it's simply redistributing inadequate coverage.

Why the Insurance Industry Isn't Rewarding Mitigation — Yet

The Regulatory Shift That Changes the Calculus

California finalized the Catastrophe Modeling and Ratemaking regulations in December 2024 — the first time insurers can use forward-looking models rather than basing rates solely on historical loss data. Under the new rules, insurers can use forward-looking catastrophe models in their rate filings. These models can incorporate mitigation variables: roof type, vent construction, siding materials, defensible space, and community-level fire risk designations.

The CDI's Wildfire Catastrophe Model Checklist, effective January 1, 2025, sets technical requirements for how these models must evaluate building features, construction materials, and mitigation measures — including specific reference to CBC Chapter 7A-compliant structures.

The Built-In Quid Pro Quo

The regulation isn't one-sided. Insurers that use catastrophe modeling or account for reinsurance costs in their rate filings must commit to writing at least 85% of their statewide market share in wildfire-distressed areas. This is the regulatory attempt to connect insurers' pricing flexibility to their obligation to remain in the market.

What the Industry Is Saying

Insurers argue they are working to incorporate mitigation into their models, but that compliance is technically complex and that the scale of recent losses overwhelms individual mitigation credits at the portfolio level. The January 2025 Los Angeles wildfires put that argument in stark relief. Estimated insured losses varied widely across sources:

| Source | Estimated Insured Loss |

|---|---|

| Verisk | $28–$35 billion |

| CoreLogic/Cotality | $35–$45 billion |

| CDI Claims Tracker (March 2026) | $23.7 billion paid across 41,800 claims |

At that scale, portfolio-level decisions feel disconnected from individual property improvements — even when those improvements are real.

What Mitigation Steps Actually Get Noticed by Insurers

Structural Hardening Matters More Than Vegetation Management

Defensible space is widely understood and legally required in many California fire zones. But it's structural hardening — the home's physical construction — that increasingly drives scores in catastrophe models and underwriting decisions.

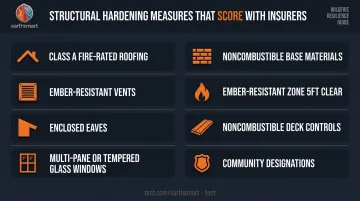

The measures that appear in both CDI's Safer from Wildfires discount framework and the January 2025 Wildfire Catastrophe Model Checklist:

- Class A fire-rated roofing — reduces ember ignition and radiant heat vulnerability

- Ember-resistant vents — one of the most common ignition pathways in wildfire events

- Enclosed eaves — eliminates a key ember entry point

- Multi-pane or tempered glass windows — resists radiant heat and direct flame

- Noncombustible materials within 6 inches of the exterior wall base

- No combustible material within 5 feet of the structure (ember-resistant zone)

- Noncombustible deck controls — decks with combustible materials underneath are a significant ignition risk

- Community designations (Firewise USA, Fire Risk Reduction Community) — factored into both discount rules and model inputs

CDI's March 2026 briefing found that community-wide adoption of the IBHS Wildfire Prepared Home Base standard reduces modeled Average Annual Loss by 31%; the Plus standard reduces it by 35%. These are community-scale effects — a single hardened home in a block of standard wood-frame construction faces a different risk profile than one in a neighborhood where multiple homes meet hardened standards.

Documentation Is Half the Battle

Insurers and catastrophe models can only credit what can be verified. Homeowners with inspection records, material specifications, and contractor documentation of completed hardening measures are better positioned — whether applying for new coverage or disputing a non-renewal.

The gap between mitigation work done and mitigation that gets recognized comes down to documentation quality. Producing a risk profile that catastrophe models can accurately score requires coordination and record-keeping well beyond standard residential construction. That's the problem earth'smart powered by tect addresses — connecting homeowners with a coordinated team and direct manufacturer input through the earth'smart powered by tectApp™ community, so every system decision is documented and verifiable from the start.

Rebuilding After Wildfire: The Moment to Materially Change Your Risk Profile

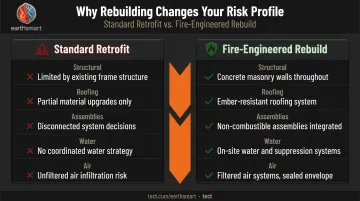

Retrofitting an existing home has real limits. You're working with an existing frame, existing penetrations, existing material decisions made under different standards. Structural hardening through retrofit is incremental improvement.

Rebuilding is different. Every system, every material, and every detail can be specified for fire performance from the ground up.

What a Rebuild Engineered for Fire Performance Actually Addresses

A home rebuilt to address wildfire risk isn't a checklist of upgrades applied to a standard frame. It's structure, envelope, and systems working as an integrated whole:

- Pre-insulated concrete masonry exterior walls that block radiant heat and direct flame — where wood framing simply can't

- Enclosed eave and long-life roofing systems with ember resistance specified at every opening

- Non-combustible materials extended to the assemblies and details that standard code-minimum builds typically leave combustible

- On-site water supply integrated with site-scale fire suppression, coordinated with structural and envelope systems from day one

- Filtered air and environmental controls that maintain habitability when smoke and ash concentrations are at their worst

The CDI's Wildfire Catastrophe Model Checklist explicitly references newer structures compliant with CBC Chapter 7A as test cases for model evaluation. A home built to this standard — and documented accordingly — is the type of structure these models are designed to score differently. That documentation advantage only exists if the decisions behind it were made correctly during construction.

Where earth'smart powered by tect Fits

For homeowners rebuilding in Pacific Palisades and surrounding high-risk areas, earth'smart powered by tect delivers coordinated architecture, engineering, and construction expertise — with direct manufacturer input through the earth'smart powered by tectApp™ community — that turns a rebuild into a permanent upgrade rather than a replacement.

Most rebuilds stall on this because architects, engineers, and material experts aren't working together when the critical decisions get made. By the time suppression integration or non-combustible specifications come up, the structural system is already locked in. Earth'smart powered by tect brings the right product experts in early — when fire-resistive assembly choices and system coordination still affect the outcome. The result is a home that can be documented, verified, and presented to insurers and catastrophe modelers with the specificity those systems require.

That level of documentation is what separates a home that meets code from one that changes your risk profile — and your options — going forward.

Frequently Asked Questions

Does hardening my home actually lower my wildfire insurance premium?

Structural hardening can influence catastrophe model outputs and rate-making under California's newer regulations, but the actual premium impact depends on your carrier, the model used, and whether the insurer is still writing policies in your area. Documentation is critical — insurers and models can only credit what can be verified.

Why are insurers still leaving California even though billions have been spent on mitigation?

Insurers manage portfolio-level capital and exposure, not individual home risk. Market exit decisions are driven by aggregate claims versus premium income — the January 2025 LA fires produced insured losses estimated between $28 billion and $45 billion, a zone-level figure that overwhelms individual mitigation credits.

What is the California FAIR Plan and is it enough coverage for my home?

The FAIR Plan is the state's insurer of last resort, offering basic fire coverage with a residential cap of $3 million — doubled from its prior limit in 2019. It does not include liability protection. In high-value markets like Pacific Palisades, the cap can leave homeowners significantly underinsured relative to actual rebuild costs.

Can I lose my fire insurance even if I've made significant fire-resistant upgrades?

Yes. California's insurance commissioner has authority over rate-making but not underwriting decisions. Insurers can decline to write or renew policies in a given area regardless of individual property improvements. Mitigation can influence your premium if your insurer stays — it does not legally prevent non-renewal outside a moratorium period.

What happens if I don't replace my canceled fire insurance?

Uninsured homeowners face full out-of-pocket rebuild costs, and lenders on outstanding mortgages can force-place expensive coverage on your behalf. Beyond the personal financial exposure, uninsured properties slow community recovery — damaged homes may sit abandoned for years, stalling neighborhood rebuilding.

Is rebuilding after wildfire an opportunity to get better insurance coverage long-term?

Rebuilding allows every material and system to be specified for fire performance from the ground up, producing a risk profile that modern catastrophe models and future insurers can score differently from a pre-fire structure.