Introduction

Homeowners insurance has become one of the fastest-rising line items in household budgets. According to the NAIC's 2022 homeowners insurance report, the average U.S. HO-3 premium hit $1,569 — an 11.26% jump from the prior year. In high-risk states, the numbers are starker: Texas homeowners were paying $3,291 on average, and California homeowners in wildfire-risk zones face both elevated premiums and shrinking availability.

For homeowners in wildfire-prone areas, the problem compounds. Around 13% of California homeowners in the highest wildfire-risk zones received non-renewal notices in 2022 alone, according to the Congressional Budget Office. That's not just a cost problem — it's an availability problem.

Yet even inside that volatile market, premiums respond to specific factors: market conditions, property characteristics, and choices homeowners make — or haven't made yet. Each of the 12 strategies below targets one of those levers, so you can bring costs down without stripping the coverage you actually need.

Key Takeaways

- Premiums have risen sharply due to natural disaster frequency, construction inflation, and location-based risk

- The biggest cost drivers: home age and condition, location, claim history, credit profile, and coverage decisions

- Effective strategies cover three areas: upfront decisions, active policy management, and reducing your home's physical risk

- Homeowners in wildfire, flood, or wind zones have additional tools, including home hardening and government-backed plans

- Cutting costs means finding where your premium is inflated relative to actual risk — not cutting coverage arbitrarily

How Homeowners Insurance Costs Build Up

Premium increases rarely arrive as a single visible shock. More often, they build gradually: annual renewal increases, endorsements added over time, coverage limits adjusted upward as home values and construction costs rise.

Cost escalation can also be sudden. A filed claim, a home's reclassification into a higher wildfire hazard zone, or a drop in your credit score can trigger a step-change in premiums that compounds at each subsequent renewal.

The Underinsurance Trap

That same cost pressure creates a counterintuitive problem: many homeowners end up simultaneously overpaying and underinsured. Research from the Philadelphia Fed, examining data from 24 Colorado homeowners insurers, found that many homeowners had dwelling coverage below 75% of true replacement cost.

Understanding the distinction matters:

- Replacement cost covers rebuilding at current material and labor prices, with no depreciation deducted

- Actual cash value (ACV) pays what your property was worth after accounting for age and wear

- Market value includes land and real estate market conditions — irrelevant to what it costs to rebuild

A policy set five years ago, before construction costs spiked, may leave you exposed at exactly the moment you need full coverage. Annual reviews close that gap.

Key Cost Drivers for Homeowners Insurance

Insurers assess your home across several risk dimensions simultaneously. Knowing what they're looking at helps you identify where you have leverage.

Property-level factors:

- Location relative to fire hazard zones, flood plains, and coastlines

- Age and condition of the roof, electrical, and plumbing systems

- Claims history attached to the property — tracked by CLUE (Comprehensive Loss Underwriting Exchange) for up to 7 years, covering claims filed by any previous owner

Policyholder-level factors:

- Credit-based insurance score (distinct from your standard credit score)

- Liability-increasing features like pools or certain dog breeds

- Type of coverage selected at inception

Some of these factors are fixed in the short term — you can't relocate your home out of a fire hazard zone or flood plain. Others are squarely within your control. The deepest, most lasting savings come from reducing actual risk exposure: upgrading aging systems, improving your claims profile, and building or rebuilding with materials that lower your insurer's expected loss. Discounts tied to policy features alone tend to narrow or disappear at renewal.

12 Cost-Reduction Strategies for Homeowners Insurance

The strategies below are organized by the type of change they require: decisions made around policy setup, active policy management, and changes to your home's physical risk profile. Effective cost reduction usually requires action across all three.

Strategies That Change Upfront Decisions

1. Shop around and compare quotes from multiple insurers

Insurers assess identical homes differently — their risk models, reinsurance costs, and appetite for certain zip codes vary. The Insurance Information Institute recommends getting at least three quotes and verifying insurer financial strength alongside price.

Don't compare price alone. Compare coverage terms precisely — a cheaper policy with a narrower definition of "replacement cost" or a higher wind deductible may cost you more at claim time.

2. Choose your deductible strategically

Raising your deductible from $500 to $1,000 may reduce your premium by 10% to 25%, according to III. That's a meaningful lever — but it only makes sense if you have cash on hand to cover the higher out-of-pocket cost when a claim occurs.

The practical rule: if you'd need to finance a loss at your chosen deductible level, you've set it too high.

3. Understand ACV versus replacement cost coverage

ACV policies carry lower premiums. They also pay less at claim time, often far less, if your roof, appliances, or systems have depreciated. For an older home where you're carrying aging systems, that gap can be substantial.

Evaluate which option matches your actual financial position. Neither is universally right — the choice depends on your home's age, condition, and your tolerance for out-of-pocket exposure.

4. Build or rebuild with resilience-rated materials and systems

For homeowners rebuilding or constructing in wildfire-prone areas, the materials and systems chosen during construction directly determine the home's insurability and premium tier. Those decisions are made before the first renewal notice ever arrives.

Homes built with fire-resistant cladding, non-combustible roofing, and upgraded electrical and plumbing systems present a lower risk profile to insurers. Earth'smart powered by tect's Earth'smart™ approach, designed specifically for Wildland-Urban Interface (WUI) construction in areas like Pacific Palisades, coordinates fire-resistive exterior wall systems using pre-insulated concrete masonry, non-combustible assemblies, long-life roofing, and integrated on-site fire suppression with a dedicated water supply independent of municipal infrastructure.

The earth'smart powered by tectApp™ manufacturer community of 70+ building product specialists ensures these decisions are made early and correctly, with direct manufacturer input at the design stage rather than during costly construction rework. That early coordination addresses the precise risks insurers are pricing for in high-risk markets.

Strategies That Change How Insurance Is Managed

5. Bundle home and auto policies with one insurer

Multi-policy bundling is one of the easiest discounts to capture, with III citing potential savings of 5% to 15%. Verify that the bundled rate is genuinely lower than purchasing separately — it usually is, but not always.

6. Proactively ask about all available discounts

Insurers don't always volunteer every discount you qualify for. At each renewal, ask specifically about:

- Claims-free history credits

- Monitored security system discounts (III cites up to 15%–20% for some monitored systems)

- Smoke detectors, deadbolt locks, and basic protective device credits (at least 5% in many cases)

- Water and gas leak detector discounts

- Storm shutters and impact-resistant glass

- Group coverage through employers, alumni organizations, or professional associations

7. Review and update your policy every year

Coverage set at policy inception may no longer reflect your home's actual replacement cost, or the current value of your personal property. At each renewal:

- Confirm dwelling coverage aligns with current construction costs

- Remove coverage for items that have depreciated out of the schedule

- Check whether any endorsements added over time are still relevant

This prevents both overpaying for coverage you don't need and being underinsured where you do.

8. Manage claim frequency thoughtfully

Filing small claims can trigger premium increases or non-renewal notices. CLUE property reports retain claims history for 7 years — meaning a minor claim today can affect your pricing through multiple renewal cycles.

Before filing, weigh the repair cost against the likely multi-year premium impact. Reserve claims for significant losses.

Strategies That Change the Context Around Your Home

9. Improve your credit-based insurance score

Most states allow insurers to use credit-based insurance scores — which differ from standard credit scores — as a pricing factor. An NBER working paper found that policyholders in the bottom credit-score quintile paid roughly $550 more annually than those in the top quintile, about a 24% premium differential.

Steps that move the needle:

- Pay bills consistently on time

- Reduce credit card balances

- Check your credit reports for errors

- Ask your insurer which bureau's data they're using

Note: Maryland and Massachusetts prohibit use of credit in homeowners insurance underwriting, so this strategy varies by state.

10. Upgrade home security and risk-reduction systems

Insurers can price improvements that reduce measurable risk. Qualifying installations often include:

- Monitored burglar and fire alarm systems

- Smoke and carbon monoxide detectors

- Water and gas leak detectors

- Smart home monitoring packages

Confirm with your insurer before investing which specific installations qualify for credits — eligibility varies by carrier.

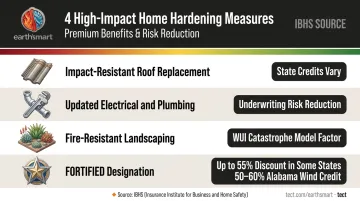

11. Harden the home against fire, weather, and water damage

Physical improvements to your home's envelope and systems can unlock meaningful premium reductions — and in high-risk markets, may be required to retain coverage at all.

High-impact hardening measures include:

- Roof replacement with impact-resistant or fire-rated materials (Texas TDI maintains a list of qualifying products for impact-resistant roofing credits)

- Updated electrical and plumbing systems — aging systems are a direct underwriting flag

- Fire-resistant landscaping — clearing dry brush in WUI zones is increasingly evaluated by insurers using catastrophe models, not just CAL FIRE designation maps

- Storm shutters and drainage improvements for wind and water exposure

IBHS reports that FORTIFIED-designation discounts can reach 55% in some states, with Alabama wind-portion credits documented at up to 50%–60% for the highest FORTIFIED tier.

For homeowners not in a position to do a full rebuild, earth'smart powered by tect's Earth'smart™ Path B advisory service works alongside your existing team to provide early system guidance, decision support, and coordination with building product manufacturers, with no full turnkey engagement required.

12. Explore government-backed plans, group insurance, and high-risk programs

In markets where private insurers have withdrawn, alternatives exist:

- California FAIR Plan: Serves homeowners unable to obtain coverage in the standard market. In the 10 counties with highest wildfire exposure, FAIR Plan policies represented roughly 22% of new and renewed residential policies covering fire perils in 2021 — up from 1% in 2015

- Texas FAIR Plan: Provides essential residential coverage for eligible homeowners when coverage is unavailable elsewhere

- Group coverage: III notes that employers, professional organizations, and alumni groups sometimes offer group homeowners insurance programs worth comparing

Check your state's insurance department for published rate comparisons and residual market options specific to your location.

Conclusion

Reducing homeowners insurance costs comes down to one thing: closing the gap between what your home actually costs to insure and what insurers charge based on perceived risk. The strategies that move the needle most are the ones that change the risk profile itself.

For homeowners in high-risk zones, the most durable path runs through the home itself. A well-built, well-maintained home with resilient systems and materials earns better coverage terms over time. Construction quality becomes a long-term financial asset, compounding in the opposite direction from the premium increases that follow standard builds.

Earth'smart powered by tect builds homes engineered to withstand fire, flood, and earthquake exposure — not just because they're safer to live in, but because they directly address the risks driving insurer withdrawal and premium escalation in markets like Pacific Palisades. A home that removes risk from the equation gives insurers fewer reasons to charge for it.

Frequently Asked Questions

What are the best strategies to lower homeowners insurance rates?

The most effective strategies fall across three areas — and addressing all three produces the most durable savings:

- Coverage decisions: shopping multiple carriers, raising your deductible strategically

- Policy management: bundling, asking for discounts annually, reviewing coverage limits each year

- Physical risk reduction: home upgrades, hardening, and resilient construction

What is the 80% rule for homeowners insurance?

The 80% rule requires you to insure your home for at least 80% of its full replacement cost. If your coverage falls below that threshold, your insurer may only pay a proportional share of any partial loss claim — meaning you absorb the difference out of pocket, even on a claim that's far below your total coverage limit.

What home improvements lower homeowners insurance the most?

Roof upgrades with impact-resistant or fire-rated materials, updated electrical and plumbing systems, fire-resistant exterior materials and landscaping, and monitored security systems consistently produce the most measurable premium reductions. In some states, IBHS FORTIFIED-designation upgrades have documented discounts reaching 55%.

Does raising your deductible significantly lower your homeowners insurance premium?

Yes. Moving from a $500 to a $1,000 deductible may reduce your premium by 10% to 25%, according to III. The strategy only makes sense if you have sufficient liquid savings to cover the higher out-of-pocket cost when a claim occurs. Without that financial cushion, a higher deductible creates exposure rather than savings.

How does my credit score affect my homeowners insurance premium?

Most states allow insurers to use credit-based insurance scores as a pricing factor. The premium gap between the best and worst credit profiles can approach 24% annually — roughly $550 per year. Improving payment history and reducing outstanding balances are the most direct levers for closing that gap.

Can living in a high-risk fire area affect my ability to get homeowners insurance?

Yes. Insurers have increasingly non-renewed or declined to write policies in wildfire-prone areas, leaving some homeowners reliant on state FAIR Plans or surplus lines carriers. Building to higher fire-resistance standards — non-combustible materials, fire-resistive assemblies, integrated suppression — directly addresses the risks driving insurer withdrawal. That's a more durable path to insurability than simply searching for a carrier willing to accept current risk.