Introduction

In January 2025, the Palisades and Eaton fires tore through Los Angeles County, burning a combined 37,469 acres — the Palisades fire consuming 23,448 acres and Eaton burning 14,021.

Together they destroyed 16,264 structures and damaged 2,051 more, with an estimated 11,000 homes lost across both fires. The displacement of thousands of households made these among the most destructive wildfires in California history.

But the fires didn't create a housing crisis. They hit a region already deep in one.

Los Angeles County had 75,518 people experiencing homelessness before the fires. The state was already short millions of homes. When tens of thousands of displaced households flooded an already-constrained rental market, the effects were immediate and severe.

This article examines what was actually lost, who bears the steepest recovery burden, why rebuilding is slower than most people expected, and what the evidence says about rebuilding smarter — not just faster.

Key Takeaways

- The Palisades and Eaton fires destroyed 16,264 structures, with roughly 11,000 homes lost — compounding a housing crisis that already affected millions of Californians.

- Renters, low-income households, and communities of color face the highest barriers to recovery and permanent displacement.

- As of late 2025, fewer than 10% of destroyed homes had rebuild permits — held back by permitting complexity, insurance gaps, and debris removal delays.

- Government funding has been committed, but most programs favor homeowners — rental recovery remains largely stalled.

- Homeowners who rebuild can construct homes that outperform what stood before: more resilient, more efficient, and built for the next 100 years.

The Scale of Loss: What the 2025 LA Fires Destroyed

Fire by Fire

The Palisades Fire destroyed 6,845 structures and damaged 975 more across 23,448 acres of coastal and canyon terrain. The Eaton Fire burned a smaller footprint — 14,021 acres — but concentrated its damage: 9,419 structures destroyed and 1,076 damaged, most of it in Altadena's established residential neighborhoods.

That distinction shapes the recovery. Altadena carries more renters, more rent-stabilized units, and fewer financial cushions than the Palisades — meaning thousands of displaced residents are waiting on landlords to decide whether to rebuild at all, not just on permits.

Rebuilding Progress Is Far Behind the Scale of Loss

According to Daily News reporting from September 2025, fewer than 10% of roughly 11,000 destroyed homes had received permits to rebuild by late September 2025:

- LA County had approved 405 permits out of 1,972 applications for unincorporated areas including Eaton

- LA City had approved 620 permits out of 1,564 applications for the Palisades area

- Malibu had issued just 2 rebuilding permits

CalMatters later reported more than 2,600 residential permits issued across Palisades and Altadena by January 2026, with 3,340 still under review. Against roughly 11,000 homes destroyed, that's still a 9-to-1 ratio of destroyed homes to active permits.

A Crisis Compounding a Crisis

The fires hit a region with no slack in the system. Before January 2025, Los Angeles County already had 75,518 people experiencing homelessness (2024 LAHSA count), a vacancy rate near zero in affordable rentals, and decades of underproduction on record. Displacing 16,000+ more households didn't create a crisis — it compounded one that had no capacity left to absorb the impact.

California's Housing Crisis Before and After the Fires

The Baseline Was Already Broken

NLIHC's Gap data shows California had just 21 affordable and available rental homes per 100 extremely low-income renter households before the fires — a shortage of approximately 1 million units. California's Department of Housing and Community Development has estimated the state needs 2.5 million new homes by 2030 and has historically produced fewer than 80,000 per year against a need of roughly 180,000 annually.

The fires destroyed housing that the market can't easily replace. Many units lost in Altadena were older, non-subsidized rentals — what housing researchers call "naturally occurring affordable housing" (NOAH). These units were cheaper because of their age and condition, not formal protections. UCLA research found that severely damaged non-rent-stabilized Altadena units had rents 17% lower than comparable undamaged units, and 40% of those severely damaged units were three- or four-bedroom homes.

At 2025 construction costs, rebuilding these units at anything near their original rent levels isn't financially viable — which means the affordable stock they represented is effectively gone.

The Rental Market Shock

As displaced households entered an already tight market, rent increases followed quickly. ABC News documented post-fire listings with asking rents 100%, 200%, and even 300% above pre-fire levels. The California Attorney General's office had sent more than 650 price-gouging warning letters to hotels and landlords and charged at least two Los Angeles realtors.

California's post-emergency price-gouging rules prohibit rent increases above 10% after an emergency declaration. Enforcement, however, has been uneven, and documented cases of gouging continue to surface in civil litigation.

The Like-for-Like Debate

Local policy has been pulled in two directions. Some county officials favor rebuilding homes identical to what existed before, prioritizing neighborhood character and streamlined approvals. State housing law, conversely, has long pushed density, ADUs, and affordability — and those two positions are now in direct conflict at the worst possible moment.

LA County's January 2025 memo requested five-year suspensions of the state's primary housing production tools in fire-impacted communities:

- SB 35 (streamlined multifamily approvals)

- Density Bonus Law (incentives for affordable unit inclusion)

- SB 9 (lot splits and duplexes by-right)

- SB 330 (housing project approval protections)

- 90-day ADU approval deadline (suspended temporarily)

The communities that lost the most housing are now operating without the legislative tools specifically designed to rebuild it faster.

Who Gets Left Behind: Displacement and Equity in Recovery

Renters are structurally disadvantaged in every wildfire recovery. They hold no equity in the property, carry no control over rebuilding decisions, and often lack the insurance coverage that helps homeowners bridge the gap. Research from the 2021 Marshall Fire found that one-third of displaced tenants were unable to return to Boulder County even years later — compared to 14% of homeowners. Altadena's experience after the Eaton Fire tracked that same pattern.

Who Was Hit Hardest

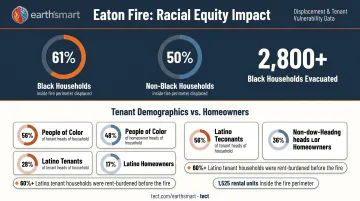

UCLA research found that 61% of Black households in Altadena were inside the Eaton Fire perimeter, compared to 50% of non-Black households. At least 2,800 Black households were forced to evacuate early in the fire.

Among tenants in the fire perimeter:

- People of color made up 56% of tenant heads of household vs. 48% of homeowner heads

- Latino householders represented 28% of tenant heads vs. 17% of homeowner heads

- More than 60% of Latino tenant households were rent-burdened before the fire

Altadena's rental stock was concentrated in the burn zone. UCLA's Latino Policy & Politics Institute found 1,525 recorded rental units in the Eaton perimeter — roughly 70% of Altadena's identified rental stock — with 927 on severely damaged properties.

Rent Stabilization at Risk

Of Altadena's 792 recorded rent-stabilized units, 545 were inside the fire perimeter. Of those, 39% were on severely damaged properties. Even when structures are eventually rebuilt, California ordinances do not automatically require rebuilt units to carry equivalent rent stabilization protections. A returning tenant can find themselves paying market rate in a building that previously protected them — the physical address restored, the affordability gone.

The Recovery Stall

UCLA LPPI found that approximately 74% of rental units in the Eaton Fire perimeter showed no publicly observable recovery action — no permit, no sale, no active listing — as of January 31, 2026. For the tenants who waited through that year, there was no timeline to hold onto — only silence from the properties that once housed them.

Why Rebuilding Is Harder Than It Should Be

Permitting and Regulatory Complexity

Governor Newsom has signed executive orders suspending CEQA and Coastal Act requirements for infrastructure repair and rebuilding. These actions have measurably accelerated some approvals — CalMatters reported single-family homes and ADUs moving three times faster than the five-year pre-fire average in some jurisdictions.

But permitting progress varies significantly by property type. The accelerated timelines largely apply to single-family owner-occupied rebuilds. Rental housing has seen almost none of the same movement, as the 74% inaction rate for Altadena rental units confirms.

That speed comes with a trade-off. By suspending SB 35 and the Density Bonus Law in fire-impacted communities, the policy prioritizes fast homeowner rebuilds at the cost of housing supply and affordability for everyone else.

Insurance Gaps and Underinsurance

California's insurance market was already in retreat before the fires. FAIR Plan enrollment in the Palisades and Eaton zones nearly doubled from 14,272 homes in 2020 to 28,440 in 2024, a 47% increase in just four years. State Farm stopped accepting new California homeowners applications in May 2023, and other carriers have followed.

The FAIR Plan's residential coverage limit of $3M sounds substantial until you price a Pacific Palisades rebuild in 2025. Many homeowners have found their policies fall short of actual reconstruction costs, particularly those who bought coverage years ago before construction costs surged.

Coverage gaps compound quickly once displacement stretches on:

- California law requires at least 24 months of ALE coverage after a state of emergency, with a possible 12-month extension

- Once those timelines expire, households pay temporary housing costs out of pocket

- Many rebuilds — especially in permitting-delayed jurisdictions — are nowhere near complete when ALE runs out

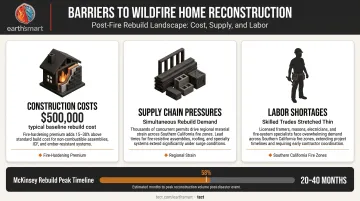

Construction Costs and Labor

A Headwaters Economics and IBHS analysis used a representative Altadena home with an estimated total construction cost of $500,000 as a baseline. Fire-resistant upgrades add real cost on top of that figure. The cost picture is further complicated by:

- Material demand: Thousands of simultaneous rebuilds strain regional supply chains

- Labor shortages: Skilled trades are stretched thin across Southern California fire zones

- Fire-hardening premiums: Non-combustible assemblies, ember-resistant venting, and Class A roofing add meaningful per-square-foot costs

McKinsey estimates residential rebuilding peaks at 20 to 40 months, with roughly 58% of homebuilding completed by that point. For most displaced homeowners, that means a multi-year wait — and that timeline assumes no permitting delays, no insurance disputes, and no contractor bottlenecks.

What Government Is Doing — and Where Gaps Remain

What's in Place

Government response has been substantial in some areas:

- HCD committed $101 million in MFSN-LA Disaster funding (announced July 2025) for affordable multifamily rental housing projects ready for immediate construction, with a preference for fire-displaced households and 55-year affordability requirements

- The State Housing Task Force was established January 20, 2025; HCD integrated with LA County's Housing Task Force on February 12

- HCD identified 723 vacant units across 141 properties from a survey of HCD-funded projects in LA County

- The Altadena One-Stop Recovery Permitting Center at 464 W Woodbury Rd. provides rebuild consultations, utility coordination, and economic recovery services

- Fee deferrals and refunds were approved for qualifying owner-occupied primary residences in unincorporated LA County

- Eviction protections covered qualifying tenants for rent due February 1 through July 31, 2025

Where Gaps Remain

Most of these tools are designed for homeowners, not rental recovery. The fee waiver program explicitly excludes commercial, multifamily, rental, and temporary housing. The $101M affordable housing commitment operates through a competitive funding pipeline — not an immediate deployment of resources. Several critical gaps remain unaddressed:

- No automatic requirement to replace destroyed rent-stabilized units with equivalent protections

- Fee waivers that explicitly exclude rental housing

- Limited enforcement of anti-price-gouging laws

- No comprehensive system to track rental displacement and recovery in real time — researchers have had to build their own tracking systems using permits, sales, and listing data

Building Forward: What Resilient Rebuilding Looks Like

For homeowners who have cleared debris, navigated insurance, and are now ready to build — the most consequential decision isn't floor plan or finishes. It's whether to rebuild what was there before, or build a home designed to perform for the next century.

Earth'smart powered by tect's Earth'smart™ program is built around one position: rebuilding isn't about replacing what was lost. It's a rare opportunity to ensure it never happens the same way again.

What Fire-Resilient Construction Actually Involves

The materials and systems that distinguish a 100+ year home from a code-minimum rebuild include:

- Pre-insulated concrete masonry (CMU), ICF, or AAC wall assemblies that combine structural performance, continuous insulation, and fire resistance in one system

- Class A non-combustible roofing — standing-seam metal, clay tile, or concrete tile with a 50–100+ year service life (vs. 15–25 years for conventional asphalt)

- Ember-resistant venting and screening throughout eaves, soffits, and attic spaces

- Tempered, dual-glazed windows and doors

- On-site fire suppression coordinated as a system: vapor dome perimeter, dedicated fire water supply, and FIREBOZZ® water cannons

- MERV-13+ filtration with ERV/HRV ventilation for clean indoor air during and after smoke events

These decisions are most cost-effective when made at the concept stage. Earth'smart powered by tect brings licensed architectural expertise and its earth'smart powered by tectApp™ community of 70+ building product manufacturers into the project early — so the right systems are specified from the design phase forward, not patched in after commitments are locked.

Three Scenarios for Rebuilding at Scale

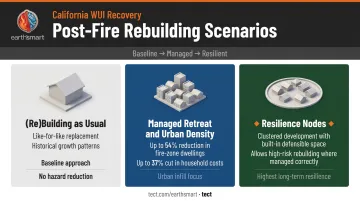

Research from Next 10 and UC Berkeley identifies three post-fire rebuilding scenarios that frame the broader choices communities and homeowners face:

- (Re)Building as Usual — historical growth patterns, like-for-like replacement

- Managed Retreat and Urban Density — incentivizes relocation from high-risk areas while promoting infill in safer urban nodes; modeled to reduce dwelling units in fire hazard zones by up to 54% in Santa Rosa, and cut household transportation, energy, and water costs by up to 37%

- Resilience Nodes — allows rebuilding in high-risk areas with clustered development and built-in defensible space

For individual homeowners, the choice between scenarios 1 and 3 is immediate. Scenario 3 doesn't just reduce risk — it changes what a home can cost to insure, maintain, and hand down. That's the case for building to a resilience standard rather than returning to the baseline that burned.

Frequently Asked Questions

How many houses have been rebuilt after the California fires?

Rebuilding progress has been slow. By late September 2025, fewer than 10% of roughly 11,000 destroyed homes had received permits. By January 2026, more than 2,600 residential permits had been issued, with 3,340 still under review. Permitting complexity, debris removal timelines, and insurance gaps are the primary reasons recovery is moving slower than expected.

How long does it take to rebuild a home after a wildfire in California?

Most rebuilds take far longer than homeowners expect. McKinsey estimates residential rebuilding peaks at 20 to 40 months, with roughly 58% of homes complete at that point. Debris removal, permitting, insurance resolution, contractor availability, and material costs all extend timelines before construction even begins.

Can I rebuild in a high fire risk zone in California?

Yes. Rebuilding in high fire risk and Wildland-Urban Interface zones is generally permitted, but new construction must meet California Building Code Chapter 7A requirements and WUI code standards for fire-resistant materials and assemblies. Given the frequency and intensity of current fire seasons, resilience-focused rebuilding is strongly recommended over like-for-like reconstruction.

Does homeowners insurance cover full wildfire rebuilding costs?

Many California homeowners carry coverage well below current rebuilding costs. FAIR Plan coverage has a $3M residential limit, which often falls short in high-cost markets. Review your coverage limits against current construction costs before breaking ground, and note that the 24-month ALE window can expire before a rebuild is complete.

What financial assistance is available for wildfire survivors rebuilding in California?

Key programs include FEMA disaster assistance (DR-4856), HCD's $101M MFSN-LA Disaster fund for affordable multifamily housing, HUD RUSH funding, LA County fee deferrals and refunds for owner-occupied primary residences, and wildfire eviction protections. Most programs prioritize homeowners over tenants. Contact LA County Recovers (recovery.lacounty.gov) or the Altadena One-Stop Permit Center for current eligibility details.